The History of Halliburton (2024 edition)

The History of Halliburton (2024 edition)

My advice for anyone looking to start an oilfield service company is this: if you want to be successful, name it after the founder.

The big three are all named after their founders.

Marcus and Conrad Schlumberger - Schlumberger

Baker Oil Tools later renamed Baker International was named after Reuben Baker and Hughes Oil Tools get its namesake from Howard Hughes Sr. His son, Hughes Jr was played by Leonardo DiCaprio in The Aviator

Halliburton was no different - founded by Earl Halliburton.

So, if you want to start a successful OFS company, name it after yourself.

Before Halliburton founded his company, he got his start working for the Perkins Oil Well Cementing Company in California, where he learned the process of cementing oil wells.

After a falling out with the owner, he packed up and moved his family to Oklahoma, where he successfully applied the new well cementing technology to jobs for Skelly Oil.

The early days were spent in the oil fields and courthouses.

Earl invented the "Jet Mixer," a more efficient way of mixing cement at the wellhead while using the methods he had learned at Perkins Oil Well Cementing.

Perkins sued Halliburton for patent infringement, but a deal was worked out in which Halliburton could use the Perkins method, while Perkins could use the new “Jet Mixer” process.

Despite the legal battles, Halliburton’s well cementing services grew rapidly, and in 1924 he formed Halliburton Oil Well Cementing Company (HOWCO), where his biggest customers became his stakeholders.

Companies such as Magnolia Petroleum (later Mobil, then ExxonMobil), Texas Company (later Texaco, then Chevron), Humble (Exxon), Sun Oil (Suncor), Pure Oil (Unocal, then Chevron), and Atlantic (ARCO, then BP) were among them.

In the beginning, Earl and his wife owned 49%, while the aforementioned oil companies and a regional bank owned the remaining 51%.

Patent infringement was abundant in the early days of the oilfield service industry, and why not, given the high levels of returns in the infant industry.

In the 1920s, Halliburton purchased the rights to an invention called the Drill Stem Tester, a device that allowed for the analysis of drilling fluid to detect the presence of hydrocarbons.

During the Depression, Halliburton invented an acidization process that helped break down oil-bearing rock formations, yielding more hydrocarbons from the reservoir.

The company added well-logging services to compete with the market leader, Schlumberger, leading to a legal battle that was eventually settled in the 1940s.

In the 1940s, the company went offshore for the first time, helping to cement a well from a platform barge in Louisiana’s Creole Field.

As wells started going deeper with higher pressures and temperatures, Halliburton had to develop a new oil well cementing technique to adapt. This led to the creation of ready-mix concrete, along with increased pumping capacity.

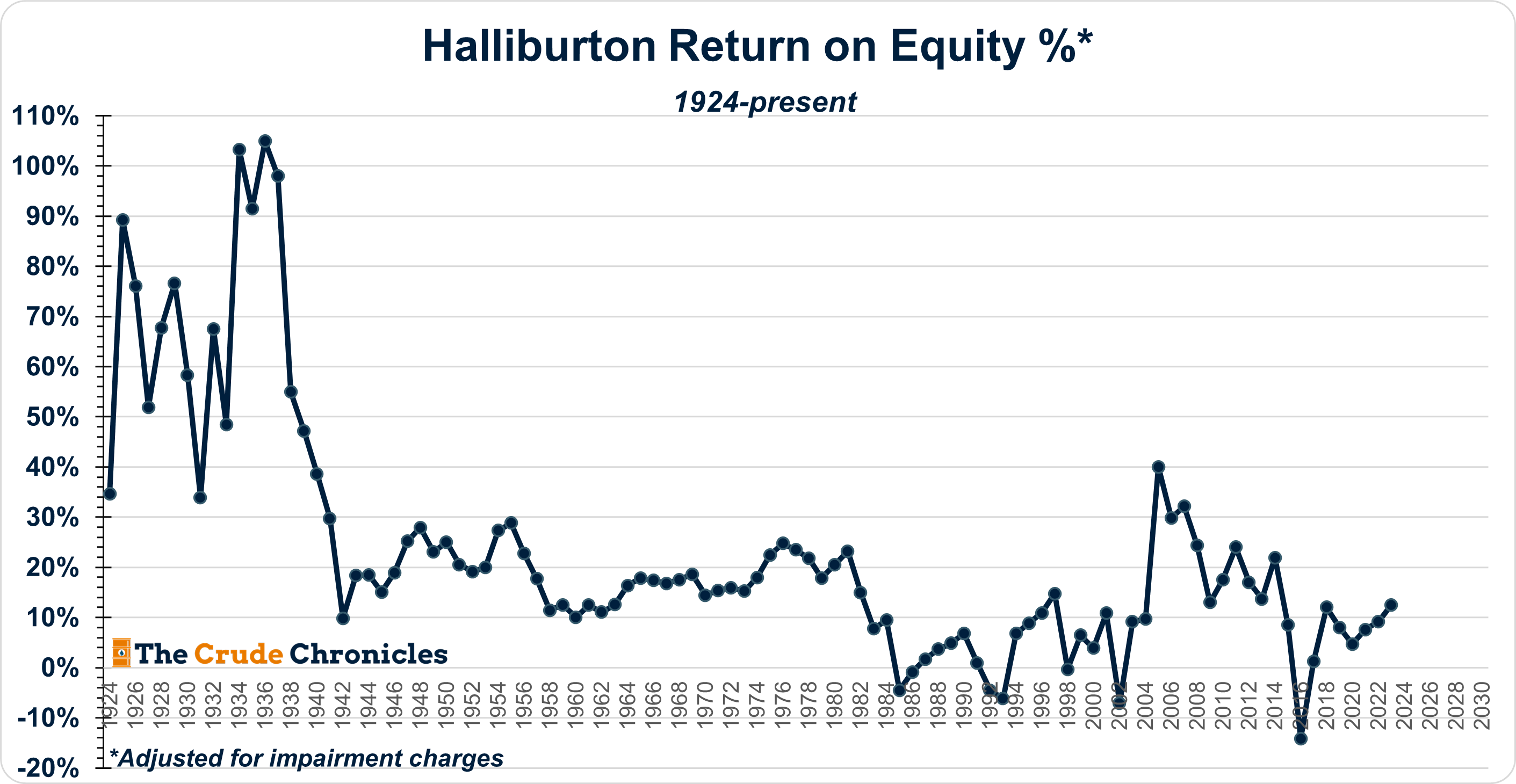

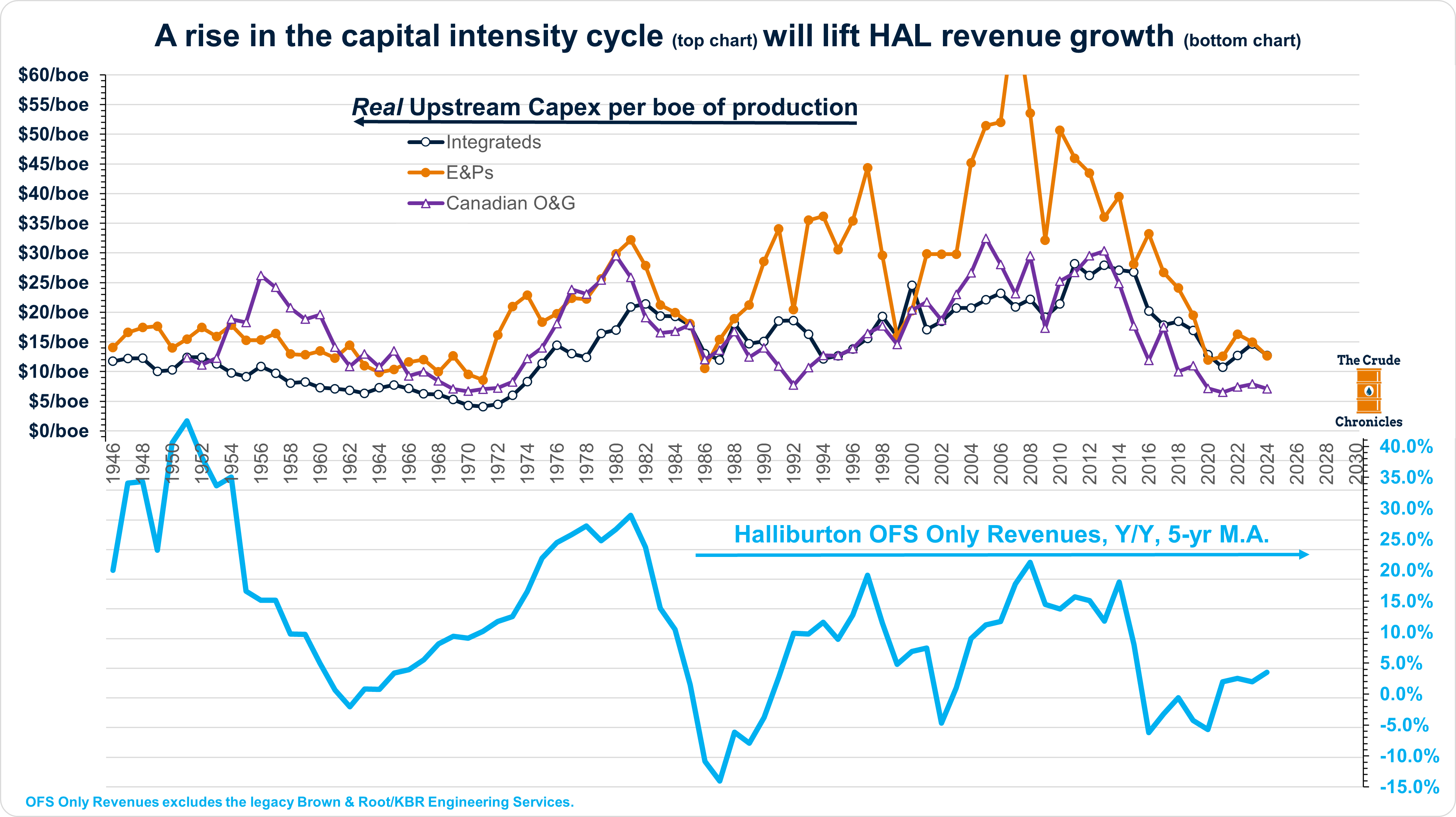

The common theme among these technological adaptations for hydrocarbons, which have become progressively harder to produce, is what I term the capital intensity cycle which in turn drives oilfield service cycles.

As hydrocarbons become harder to produce, the capital intensity cycle picks up. As the cycle intensifies, producers require newer and better services, benefiting companies like Halliburton.

However, high returns bring more competition. With increased competition, it becomes a race to the bottom as the industry finds ways to boost well productivity while lowering costs. This was evident during the shale boom—where the zipper frac was eventually replaced by the simul-frac (HERE), among other innovations. This is the environment Halliburton (HAL) has been navigating since the rise of North American shales, as shown below.

Keep reading with a 7-day free trial

Subscribe to The Crude Chronicles to keep reading this post and get 7 days of free access to the full post archives.