A Defensive Rally.

The Gist: It remains a “risk off” rally but the gap continues to close between O&G equities and the market.

Hey gang — I’m back from Cancun where a week of poolside drink service does wonders to reset the brain waves.

But back to reality.

Energy stocks have been on a year-to-date tear, leading all S&P sectors. If I had told you a year ago that we would go through a trade war, that every major oil agency would be forecasting record surpluses, and that Venezuela would be open again for business — all while oil prices were down double digits — you likely would not have expected most oil & gas indices to be making all-time highs.

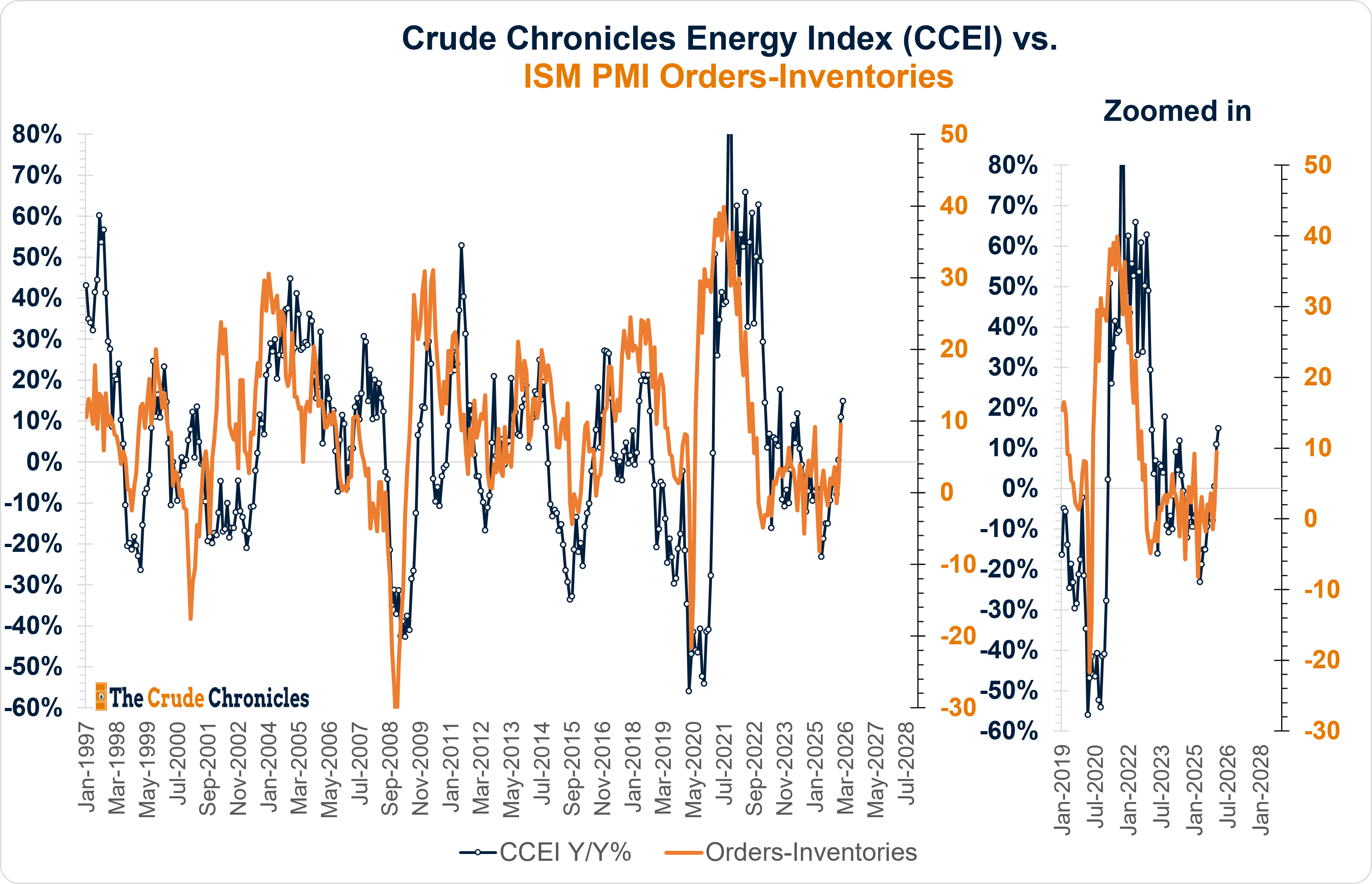

What’s different this time is that momentum has improved alongside strengthening global manufacturing PMIs, as evidenced by an uptick in leading indicators such as the ISM Orders/Inventories.

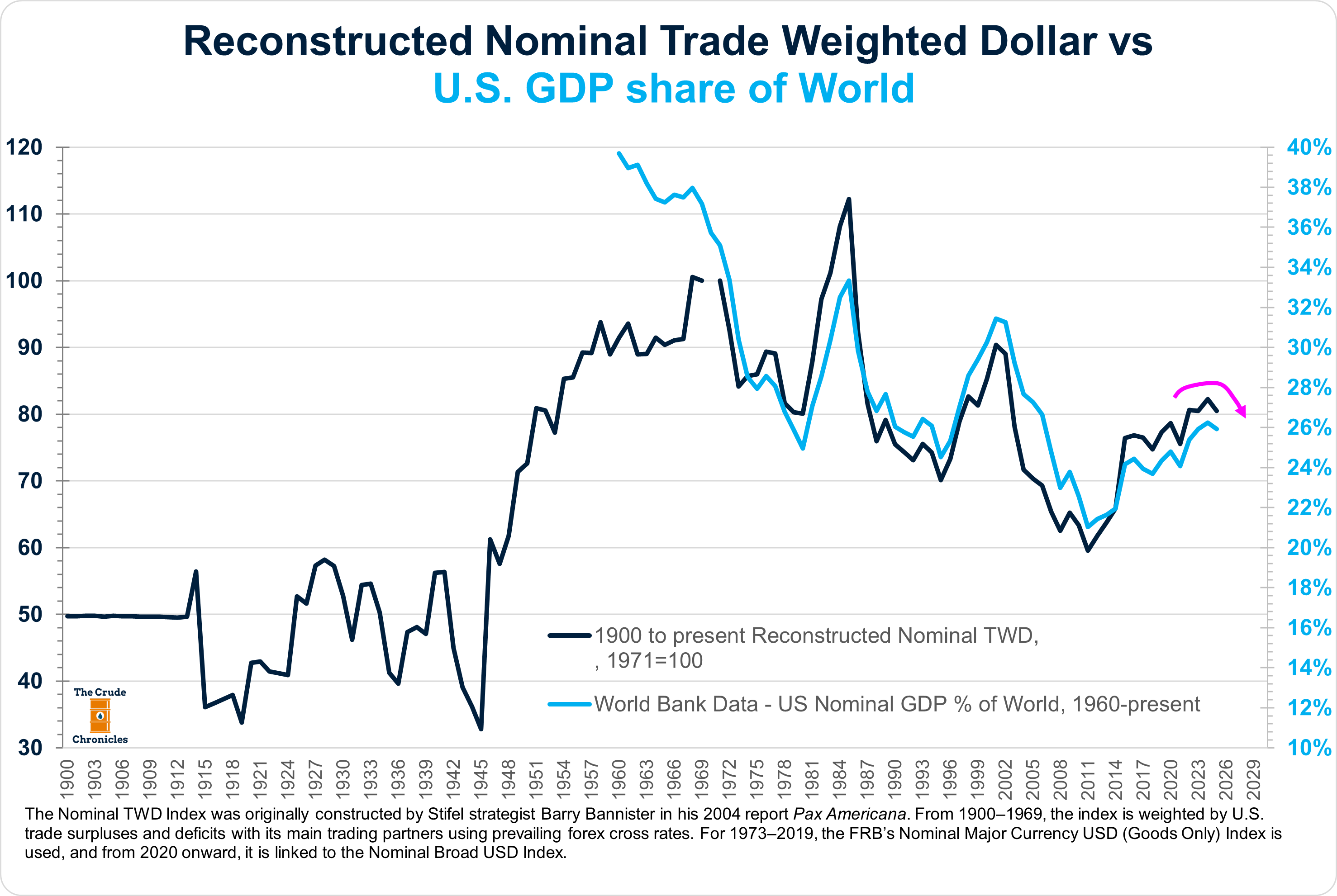

Couple that with U.S. dollar weakness, as overseas markets continue to outperform U.S. equities and investors increasingly question the capital allocation strategies of U.S.-centric Mega Tech. (HERE).

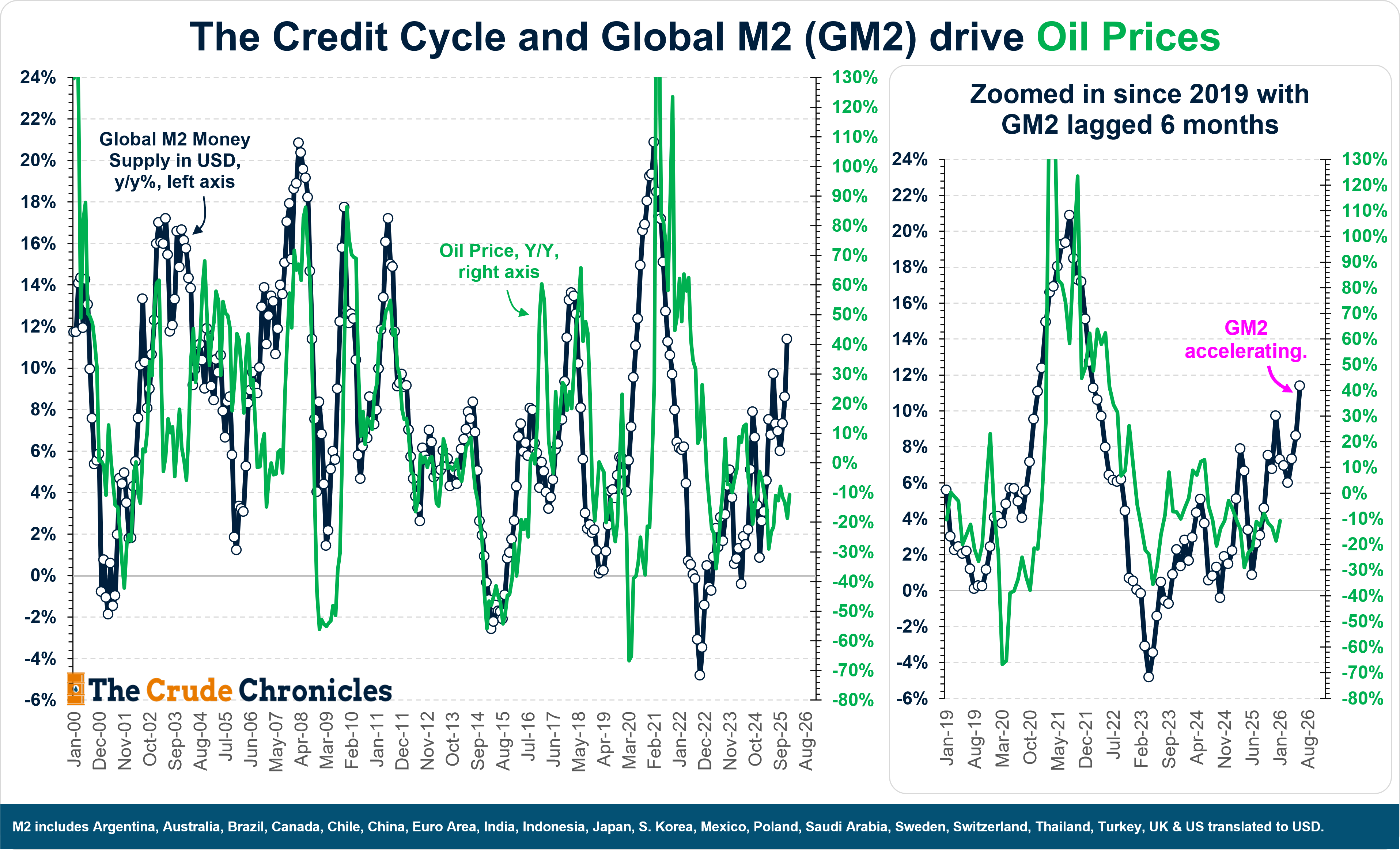

The global credit cycle as measured by global money supply in USD is fairing well - which is supportive of overseas GDP and future oil demand. The problem for oil markets is not just a supply side argument but a lack of EM demand the last few years. EM demand is in the early stage of a recovery.

Another explanation for the recent outperformance is the sector is a risk off trade that began in the depths of COVID: sector-observed betas — a measure of relative volatility — have been steadily declining.

In strong, momentum-driven markets, energy has tended to lag. However, when the broader market faces headwinds, energy has increasingly behaved like a defensive sector and outperformed.