ConocoPhillips: From Standard Oil to The Standard in Returns - A financial history revisited

The Gist: The first half of this post is a very brief history of ConocoPhillips. The second half shows how COP is once again growing reserves at a reasonable price (F&D) which may be the playbook for the entire industry going forward.

When we think of the descendants of Standard Oil most think of ExxonMobil and Chevron and possibly the N. American refining assets of BP (Amoco/Standard of Indiana & SOHIO).

Not many of us think of ConocoPhillips, and to be more specific, the Conoco part or as it was previously known, Continental Oil Company.

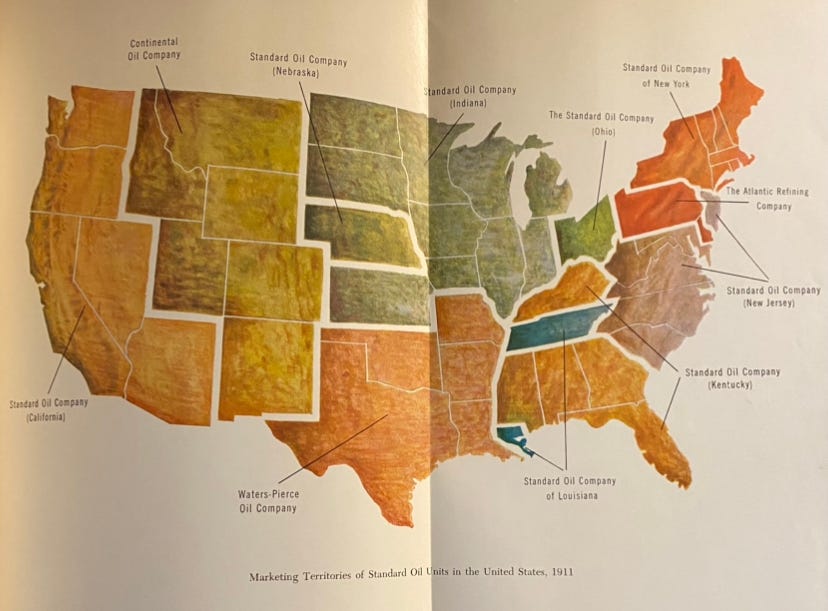

After the breakup of Standard, Continental Oil was one of the smaller descendants.

Under the monopoly, its marketing domain extended from Montana to New Mexico, where the population density was significantly lower than in other parts of the country, and upstream production was scarce.

Conoco would get its start in E&P when it was merged with Marland Oil, a MidCon producer that was growing aggressively. Marland and Conoco were both financially backed by the House of Morgan. When Marland came under financial strain, Morgan would amalgamate the two. Conoco would adopt Marland’s branding for the next 40 years.

Frank Phillips (HERE), the founder of Phillips Petroleum, began his career as a banker providing capital to drillers during the MidCon oil boom of the early 20th century.

He would go on to form Phillips Petroleum.

What makes Phillips Petroleum particularly intriguing is that it managed to remain independent and was never acquired by a larger integrated oil company or financial backer back east.

This can not be said of all the early 20th-century oil pioneers in Oklahoma and Texas.

Humble Oil was purchased by Standard of NJ.

Gulf Oil was taken over by the Mellon family in PA.

Magnolia Petroleum was acquired by Standard of NY.

Joseph Cullinan lost control of Texaco to money interest back east.

Marland Oil as previously mentioned would fall under the control of JP Morgan.

But not Phillips Petroleum.

We can draw parallels to the wave of M&A presently taking place in E&P land. Many have come, but few will remain.

Other observations are very unique to the DNA of ConocoPhillips.

First, when examining the history of the oil majors, many of them, along with the companies they acquired, had production concentrated in the Middle East.

When a wave of nationalization swept through the industry in the 1970s their control of the commanding height would fall from 55% of global oil production to less than 8% today.

But ConocoPhillips’ history is different.

A reconstructed production chart looks much different than the others as evidenced below.

Keep reading with a 7-day free trial

Subscribe to The Crude Chronicles to keep reading this post and get 7 days of free access to the full post archives.