Energy vs. Tech - The Shareholder Value Bet

Energy vs. Tech - The Shareholder Value Bet

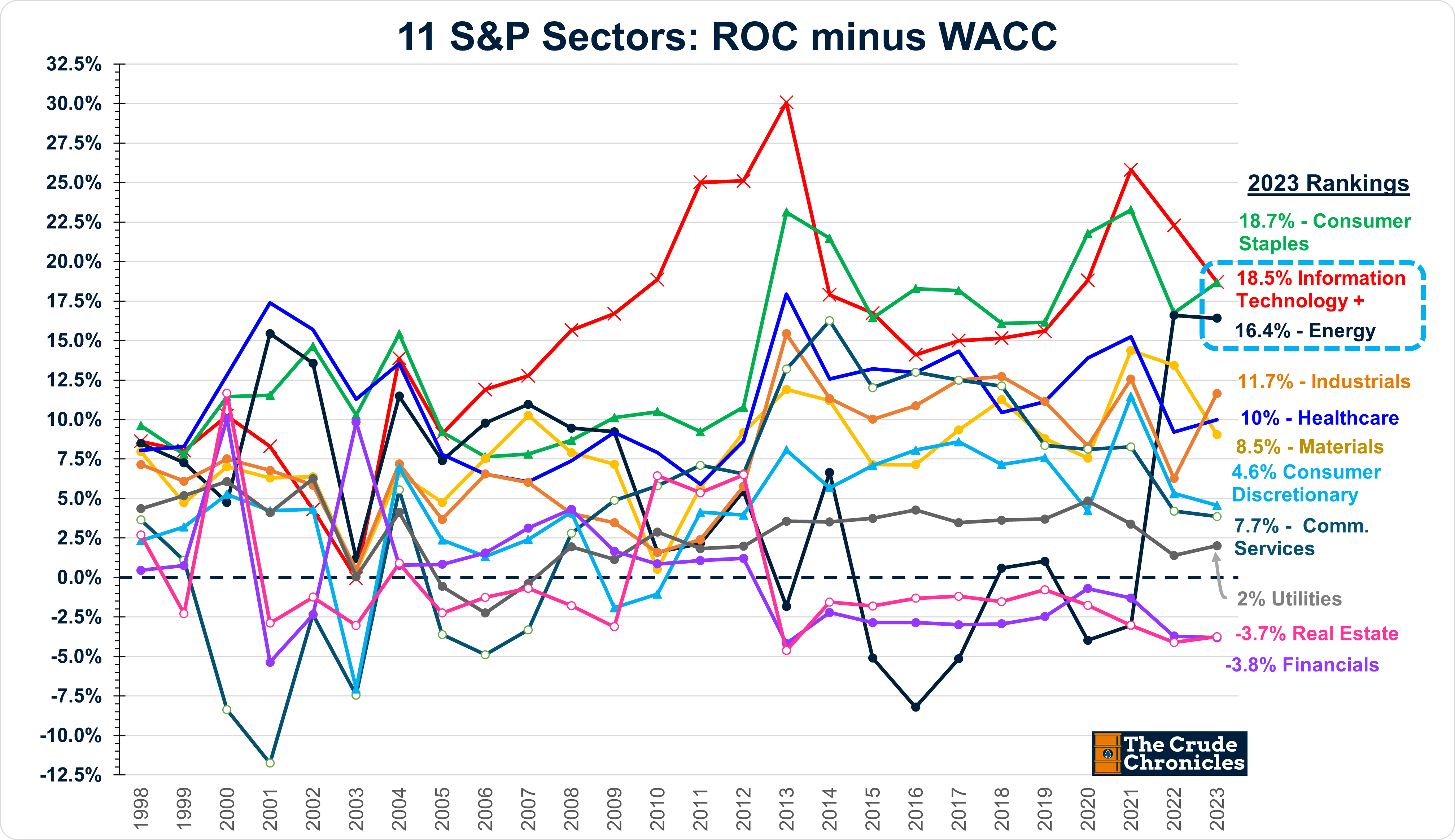

The Gist: (1) Energy’s shareholder value (return on capital minus costs of capital) is approaching that of the market’s beloved “Tech+” sector. (2) The industries within the energy sector return rank among the top in terms of shareholder returns. (3) However, Tech+ has a growth component that energy can’t match. So much growth that expectations are beginning to stretch beyond reasonable bounds.

This week's post is brief, yet it continues the theme of return on capital, which I've been consistently addressing as we receive full-year 2023 results.

For this article, we won't be utilizing my datasets; instead, we'll be relying on the data compilations assembled by Aswath Damodaran, the valuation expert from NYU. (HERE).

What I find particularly intriguing about his yearly update is that the Energy sector is narrowing the difference with the highly favored Tech+ sector regarding earning a return on capital that exceeds its cost, as demonstrated below.

Lower energy prices can impact returns but so can an excessive amount of investment.

On the subject of investment, energy is still middle of the pack whereas IT+ is second to the inherently capital-intensive Industrials sector as shown below.

Keep reading with a 7-day free trial

Subscribe to The Crude Chronicles to keep reading this post and get 7 days of free access to the full post archives.