ExxonMobil: The Comeback (Part 1: Into the Abyss)

ExxonMobil: The Comeback (Part 1: Into the Abyss)

A Financial History, 2024 Edition

You may have inadvertently received this post a few days ago. There was a technical difficulty.

The Gist: This is the first in a three-part series on ExxonMobil’s financial history now that the Pioneer deal is closed. I chose the title "The Comeback" because, just like the bellwether, I also have to make a comeback. I want the Crude Chronicles to be known for the long-term historical data and perspectives on the O&G cycles and the companies involved, which is what the overwhelming majority of my audience finds valuable in my content and what differentiates me. Lately, I have been straying from the histories. So, just like XOM, I am making a comeback and steering this ship back on course. June 1st will mark my one-year anniversary of going paid and making this my full-time gig, the perfect time for a slight course correction.

Part 1 is titled “Into the Abyss” and will retrace the COVID lows, draw some parallels to XOM’s past and take us up to the 1970s.

Part 2 will address the period from the 1970s to the present.

Part 3 will address the period from the present to the possible future.

Programming Note: Also, there will be no post on Tuesday due to the Memorial Day holiday. See you in a week.

Let’s begin.

Part 1 - Into the Abyss.

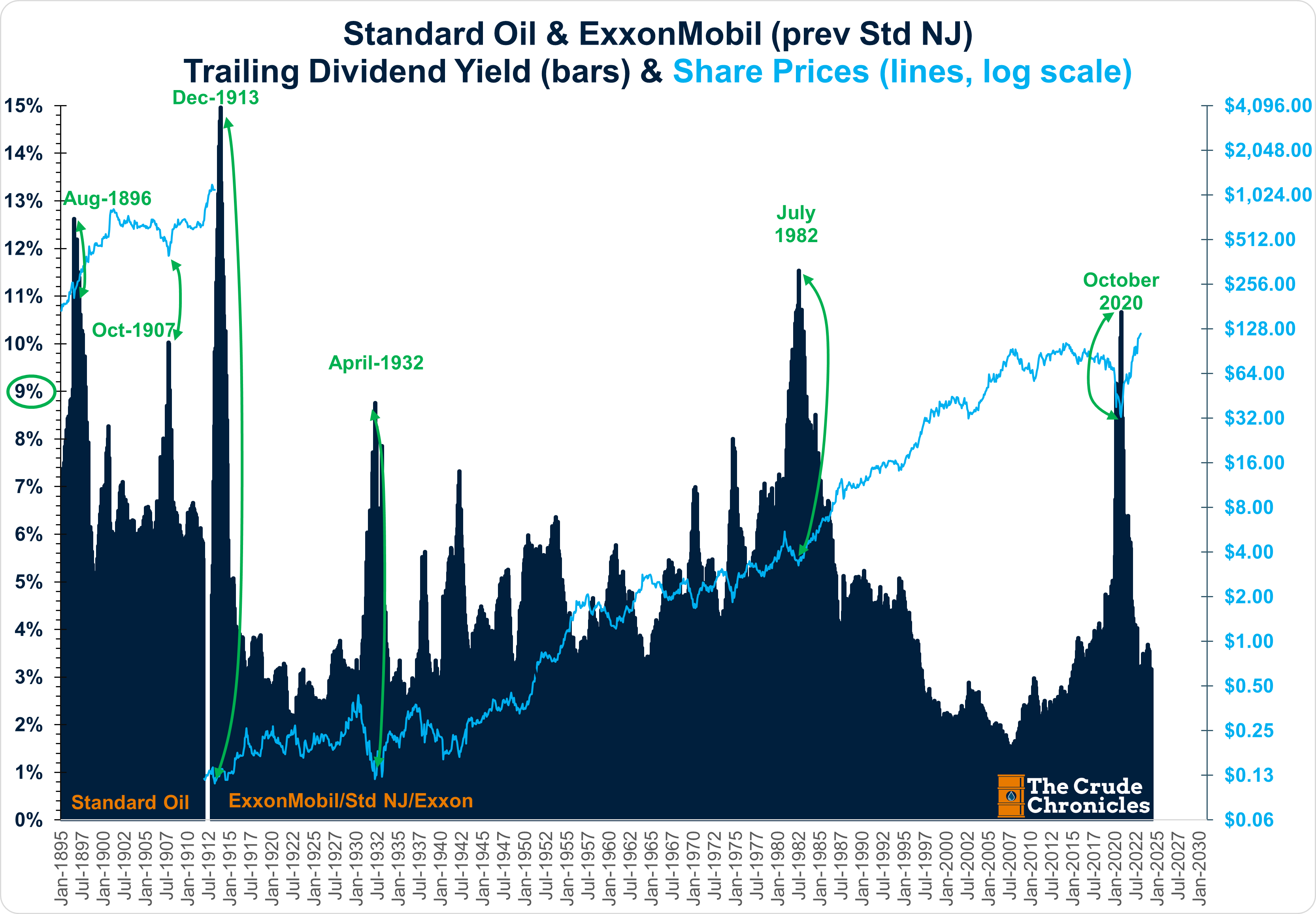

Nothing better defines the dismal times ExxonMobil was facing a few years ago than its dividend yield.

In the land of big oil, a 9% dividend yield is a rare event and often a sign of weakness rather than strength.

Observing the above chart, any student of financial history will recognize the events surrounding these six periods in which XOM’s yield surpassed 9%. Two of them involved a collapse in energy prices, and five were due to a breakdown in financial markets. The events of October 2020 were a mixture of both.

Yet to the astute observer, what I try to point out is that these events have also turned out to be a once-in-a-generation entry point for the shares, dating back to its predecessor Standard Oil.

In 2020, the risk was that XOM might go the route of other rivals and cut the dividend.

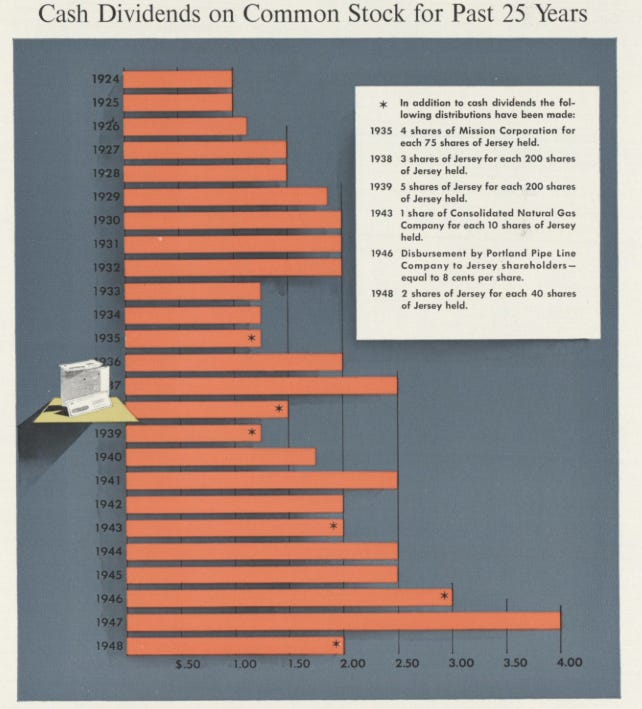

As the graphic below shows, not since 1948 has XOM or its predecessor, Standard Oil of New Jersey, needed to cut the dividend.

Yet 1948 was different. There was no market panic to speak of; rather, Standard Oil of New Jersey was set to purchase a 30% stake in ARAMCO, so capital was being allocated to the greatest prize the oil world has ever found.

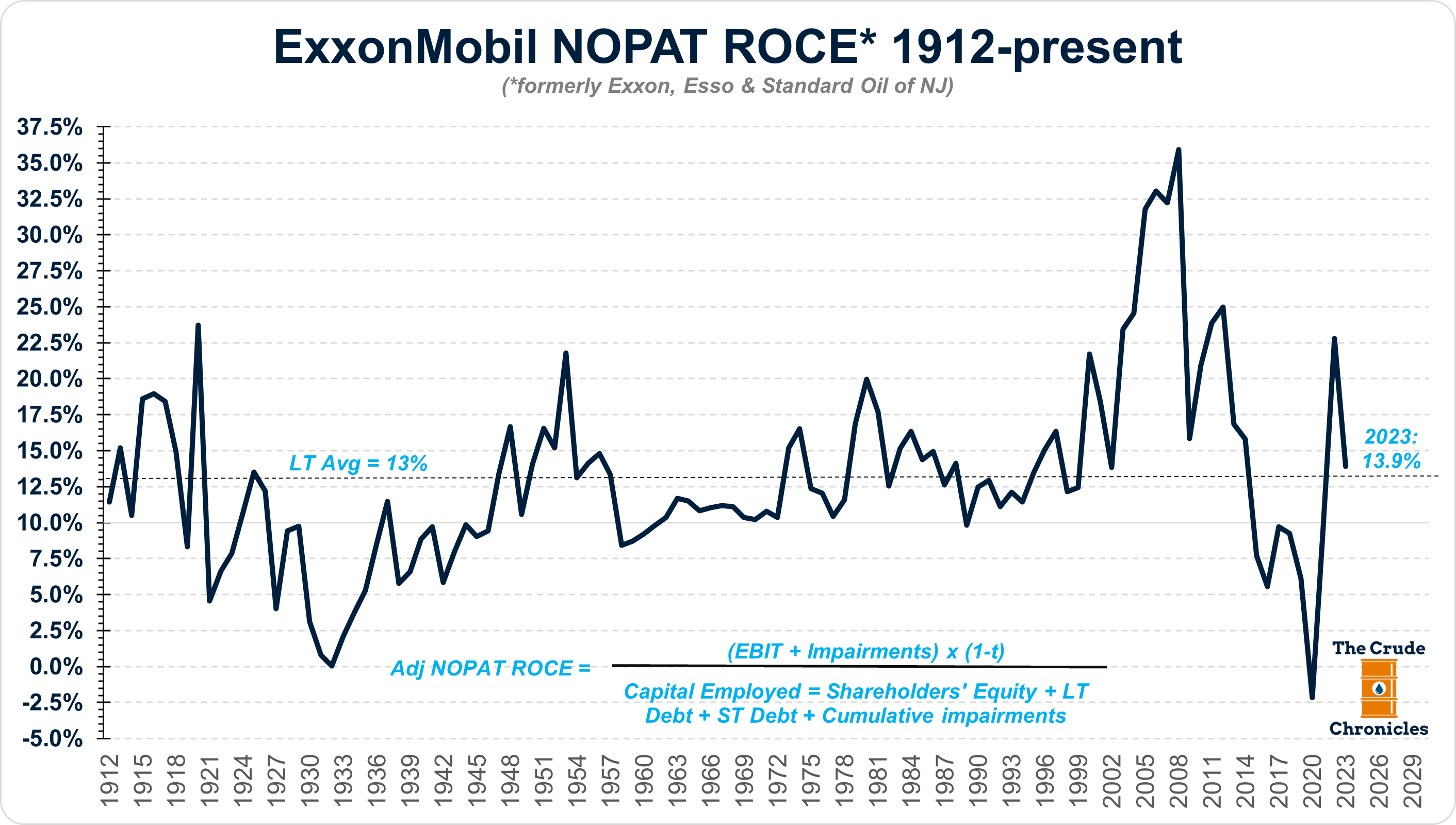

Going back to the days of Rockefeller, the descendants of Standard Oil had never lost money.

Profits rose and fell over the years, but they never went negative.

In 2020, they broke the buck.

The ever-important metric of returns on capital had reached an all-time low as well.

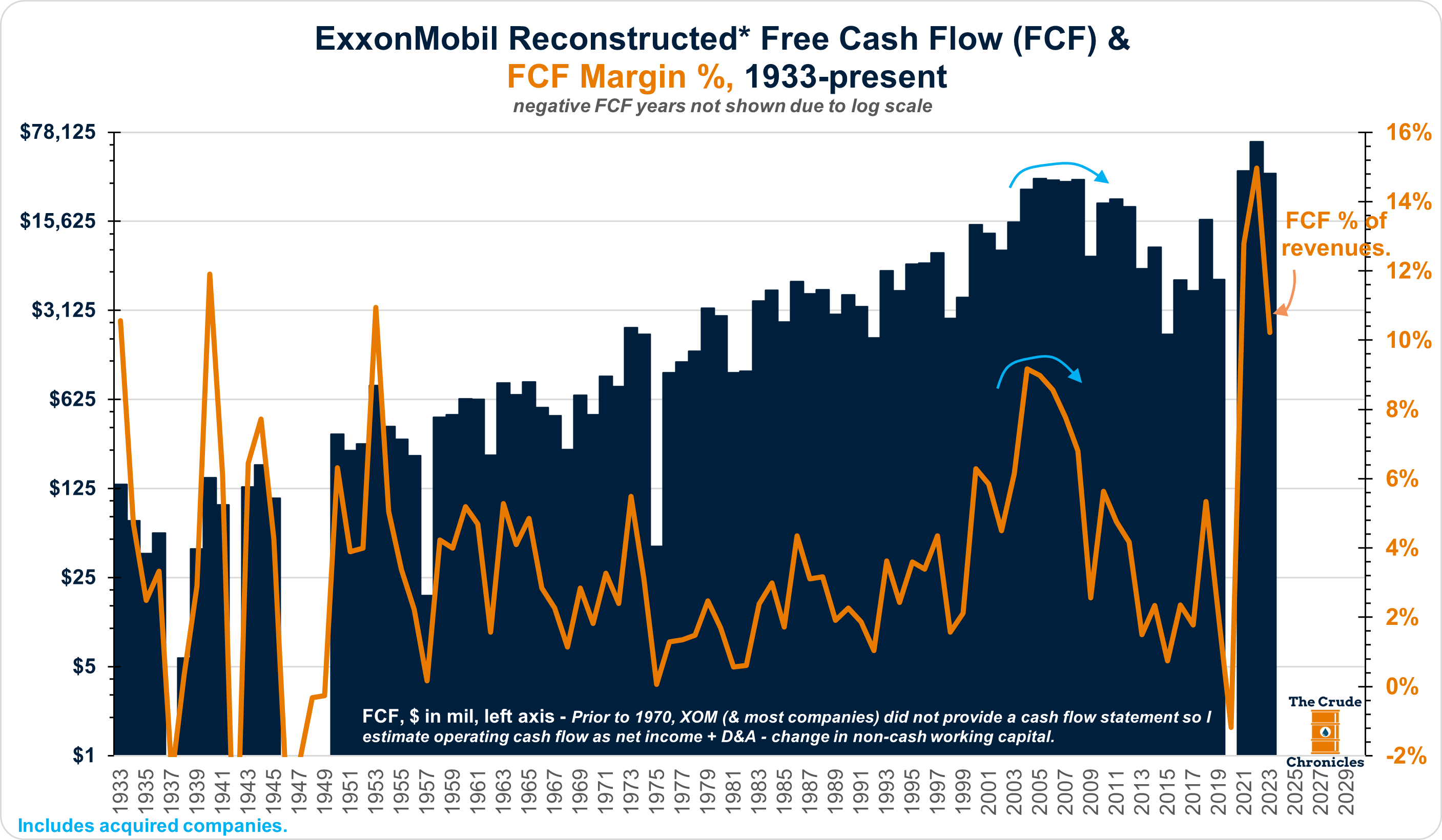

Free cash flow had been in decline since its peak in the mid-2000s.

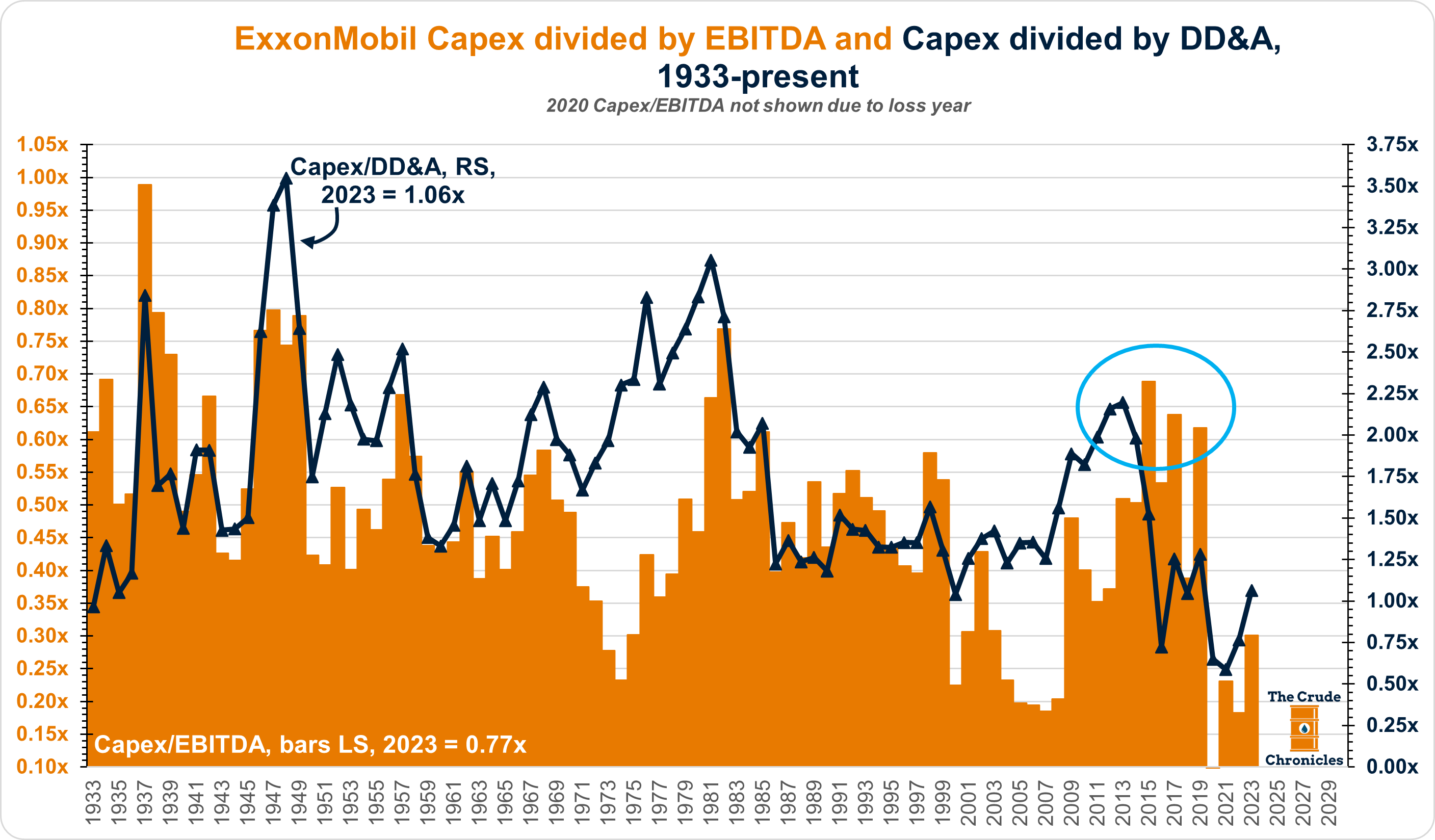

Capital spending had gotten out of hand as well.

With very little to show for in the way of production growth.

Keep reading with a 7-day free trial

Subscribe to The Crude Chronicles to keep reading this post and get 7 days of free access to the full post archives.