Incentivizing Refiners over Chipmakers

(2025 U.S. Refining Compensation Review)

The Gist: The U.S. refining industry has incentive structure characteristics that the rest of the industry should mirror. Despite some near term seasonality headwinds, these incentive structures will continue to lead to proper capital allocation and outperformance vs. other high flying sectors.

Refining stocks have become a consensus long, and we’re hearing more and more podcasters and commentators talk about them.

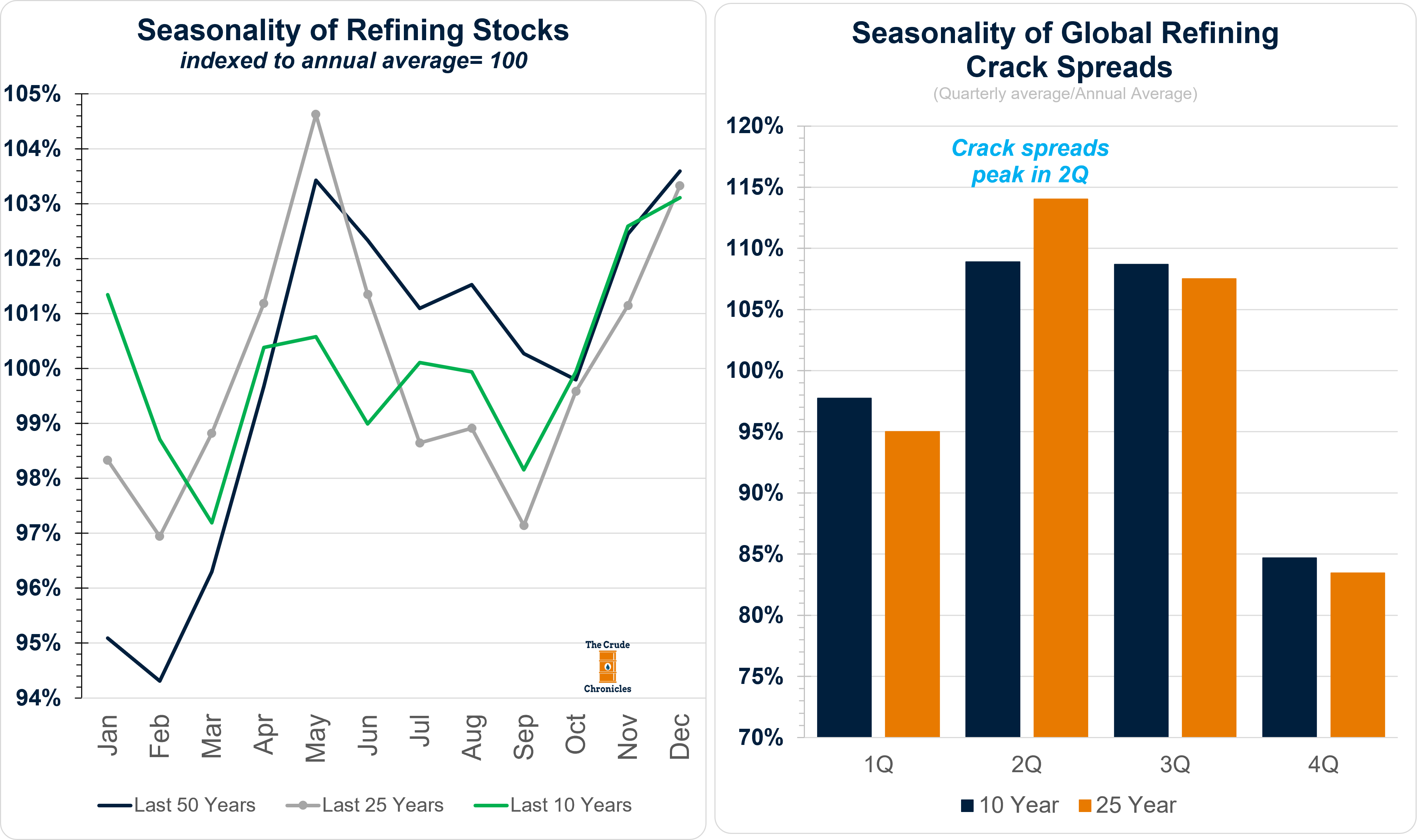

But keep in mind—they are entering their seasonally weak period from May through September/October, as crack spreads typically peak this quarter.

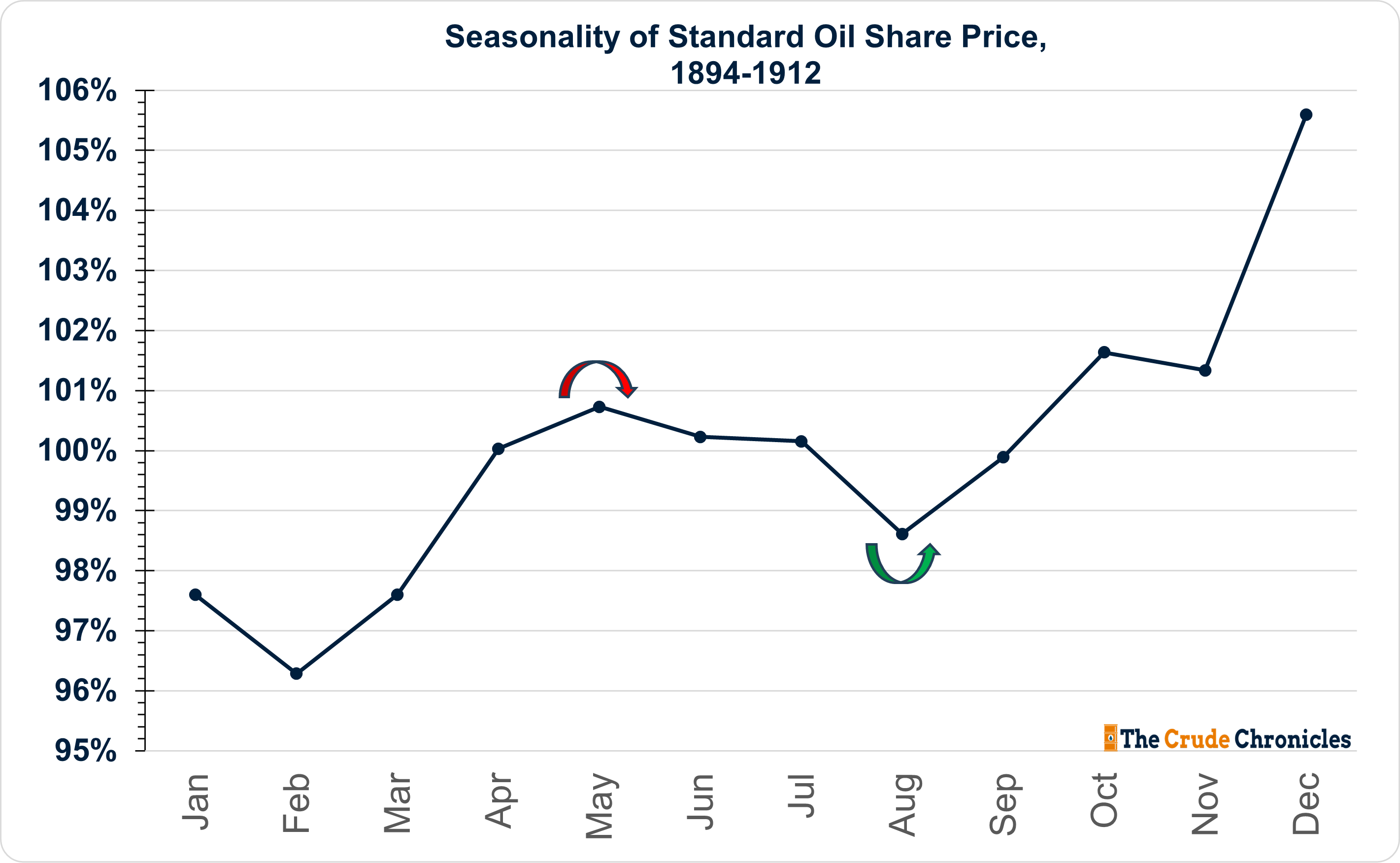

Even Rockefeller’s Standard Oil refining monopoly had a degree of seasonality.

One of the best refining analysts we know used to call it “Straw Hats in Winter.”

In the winter, inventories are typically low, demand begins to rise seasonally, and spring turnarounds take capacity offline—all of which tightens refining margins. This year we can also add Straits of Hormuz closure and a lack of medium/sour crudes to the list of seasonal strength.

In response, analysts raise estimates, but stocks are ahead of it and the trade repeats once again the following year.

It’s May, and estimates are moving higher.

Seasonality is more common in this industry than “ceasefires” are in the crisis.

But there’s more to the refining story than just the Straits of Hormuz and the record crack spreads.

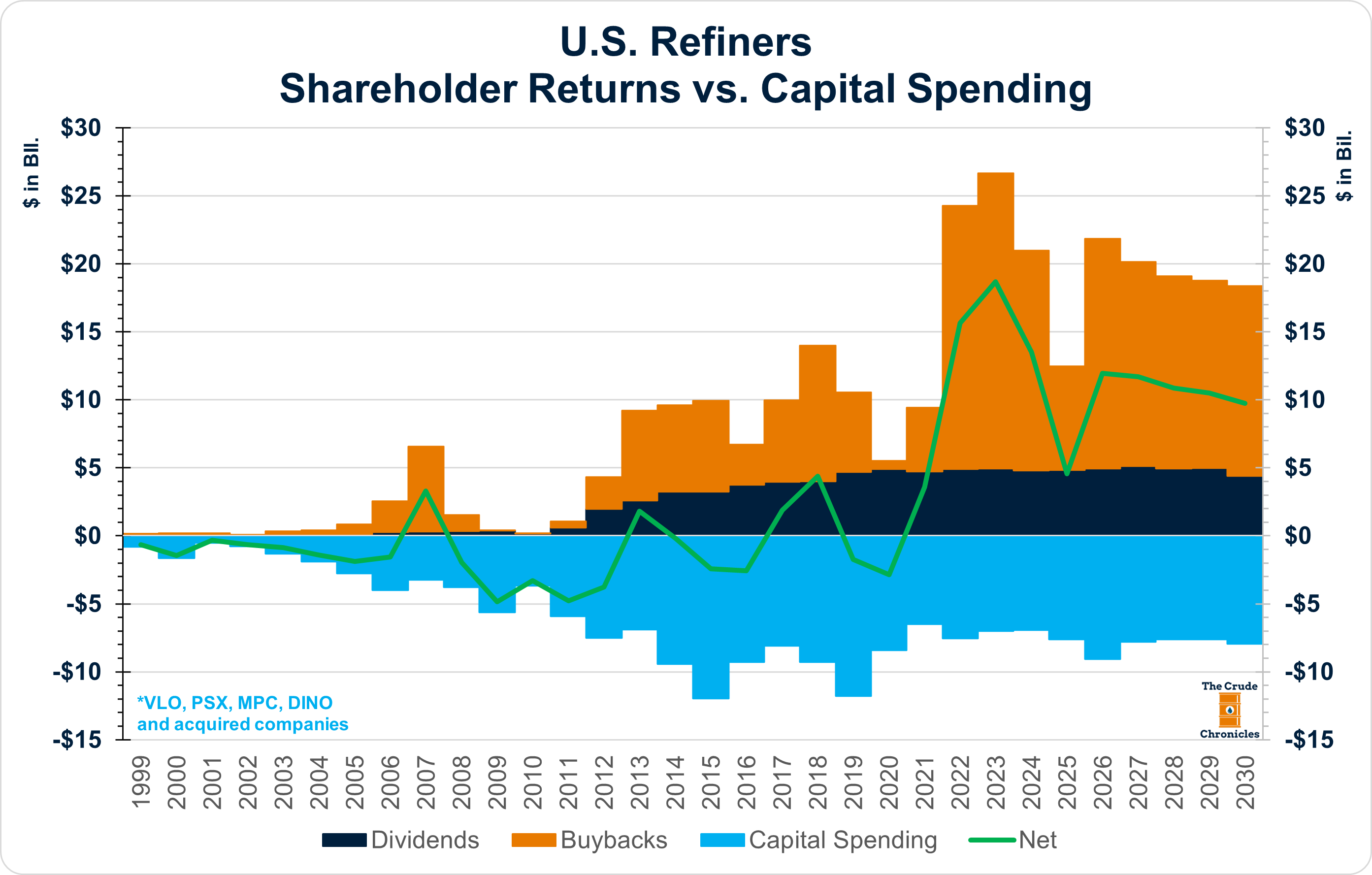

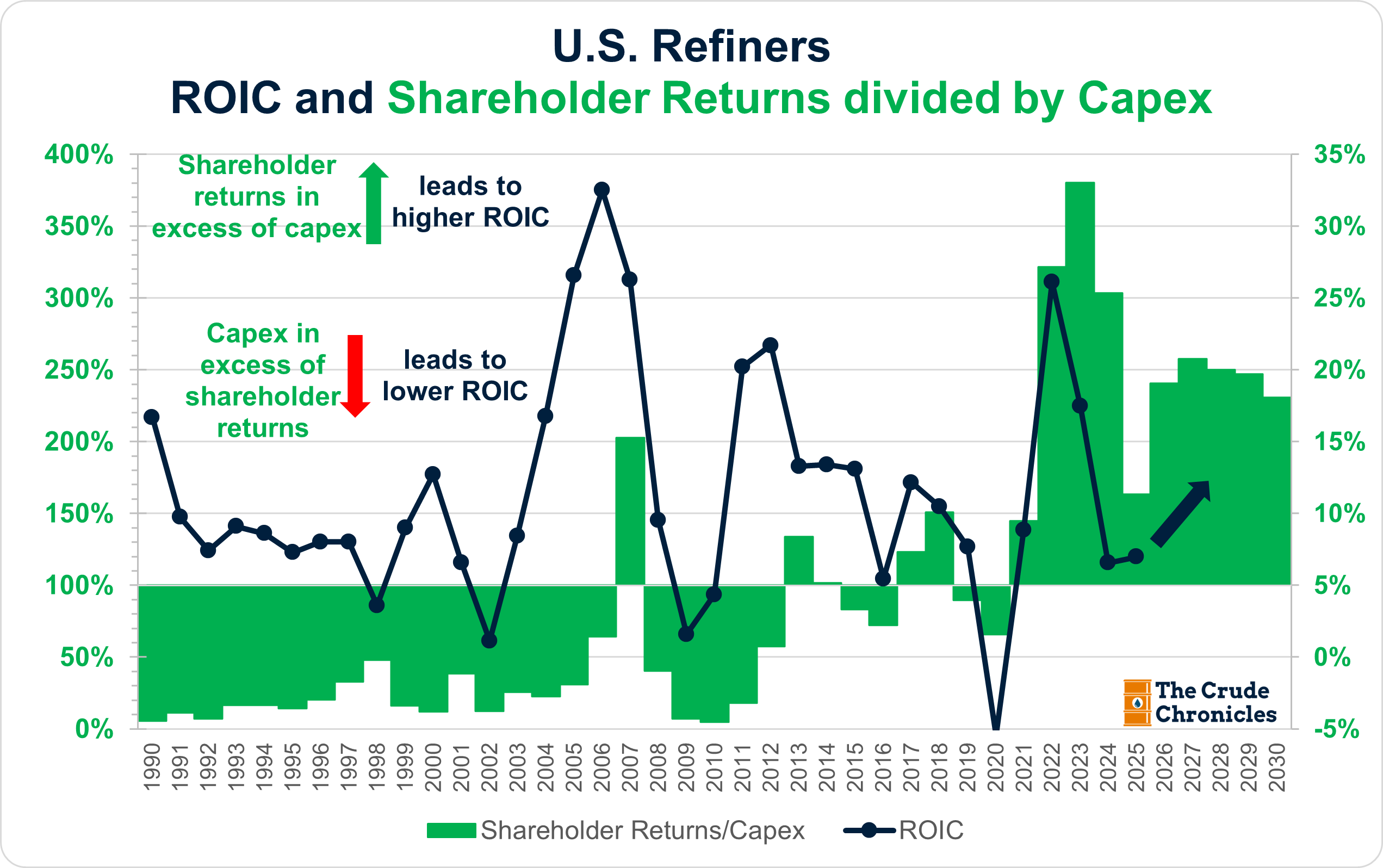

Despite being viewed as a capital-intensive industry, refiners have the best capital discipline in oil & gas. In fact, they’ve become so capital-light that they consistently return more cash to shareholders—via dividends and buybacks—than they require for reinvestment.

As the chart below shows, this trend has only accelerated over time.

This has led to structurally higher ROICs than in prior cycles.

But U.S. refiners didn’t get here overnight. They went through a boom-and-bust cycle in the 2000s that ultimately led to better corporate governance, improved incentive structures, and a stronger industry overall.

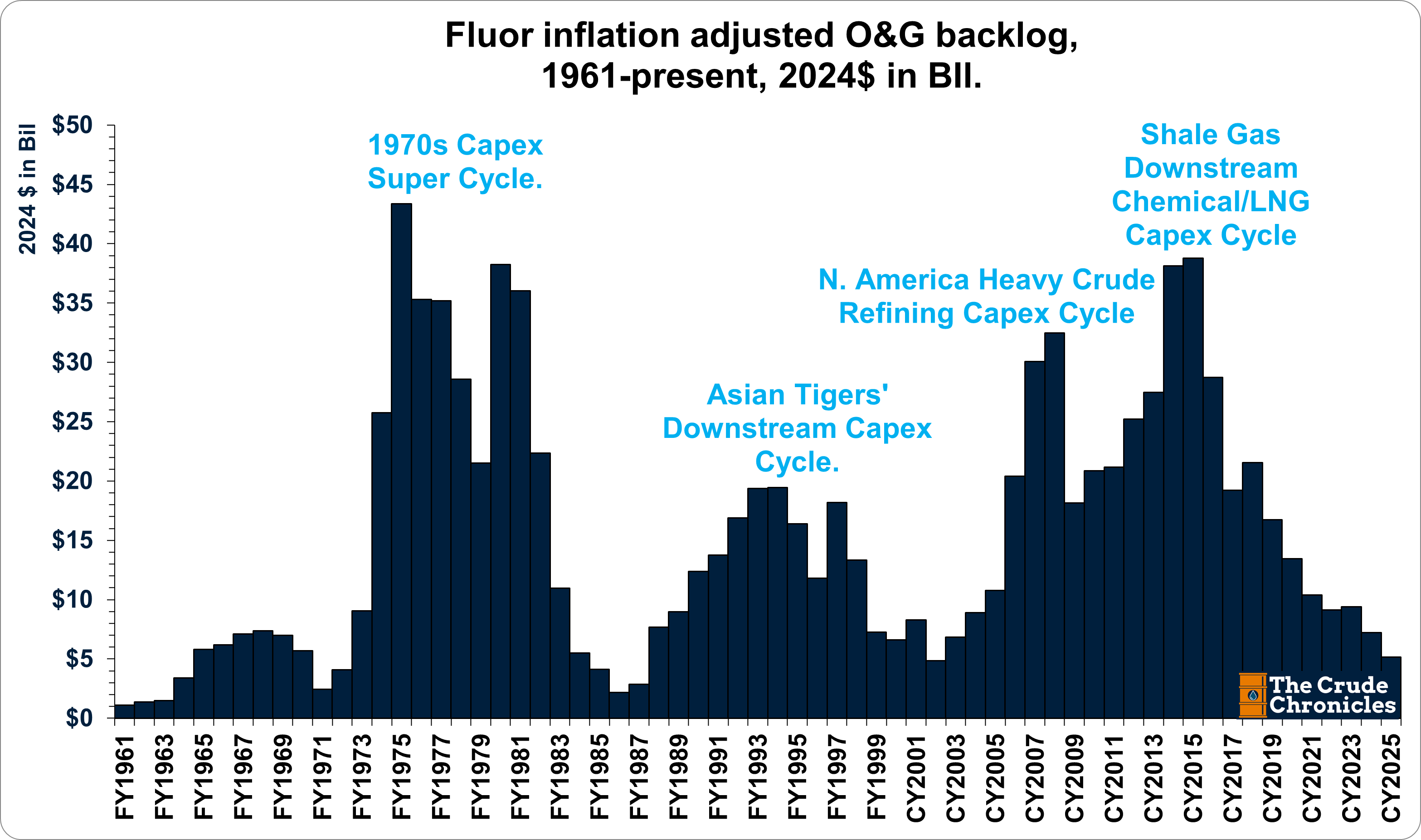

I got my start on the sell side covering EPC firms that benefited from downstream O&G capital spending themes. Names like Fluor, Foster Wheeler, Jacobs Engineering, Chicago Bridge & Iron, and KBR—large project managers whose edge was executing complex EPCm projects.

Of those names, only two remain public today (Fluor and Jacobs), and just one is still meaningfully tied to oil & gas—a reflection of the industry’s cyclical booms and busts.

The 2000s were a glorious period, as the U.S. pushed to expand refining capacity wherever possible.

Marathon was expanding and upgrading its Garyville and Detroit refineries. Total and Motiva (the Shell–Aramco JV) were both investing heavily in their Port Arthur refineries. Valero had a long list of projects—the Port Arthur coker, St. Charles hydrocracker, Corpus Christi, and more.

It was an easy time to be an EPC analyst. Estimates and price targets were up and to the right.

But one lesson stuck with me:

When an industry is pushing EPC firms’ book-to-bill ratios to ~1.4x, it’s a sign that capital discipline is breaking down—and a reckoning isn’t far behind. Every single one of the investment manias portrayed below ended in a bust. Every single one!

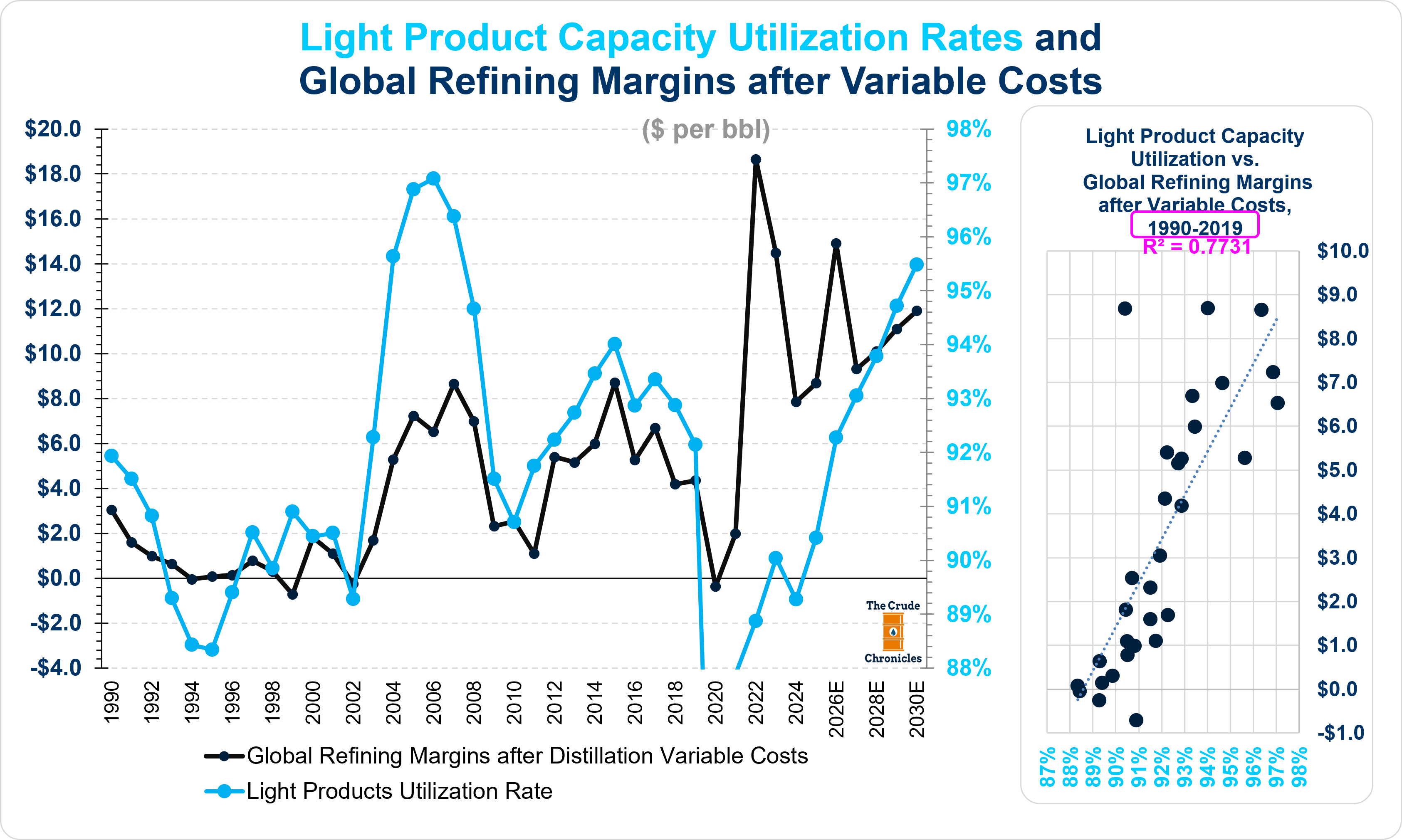

All of the refinery projects described above were designed to capitalize on two key dynamics: the growing availability of heavy/sour crude that the U.S. was increasingly reliant on, and the ability to maximize output of light products such as gasoline, jet fuel, and diesel.

But by 2006, light product capacity utilization—also known as secondary or upgrading capacity utilization—had peaked.

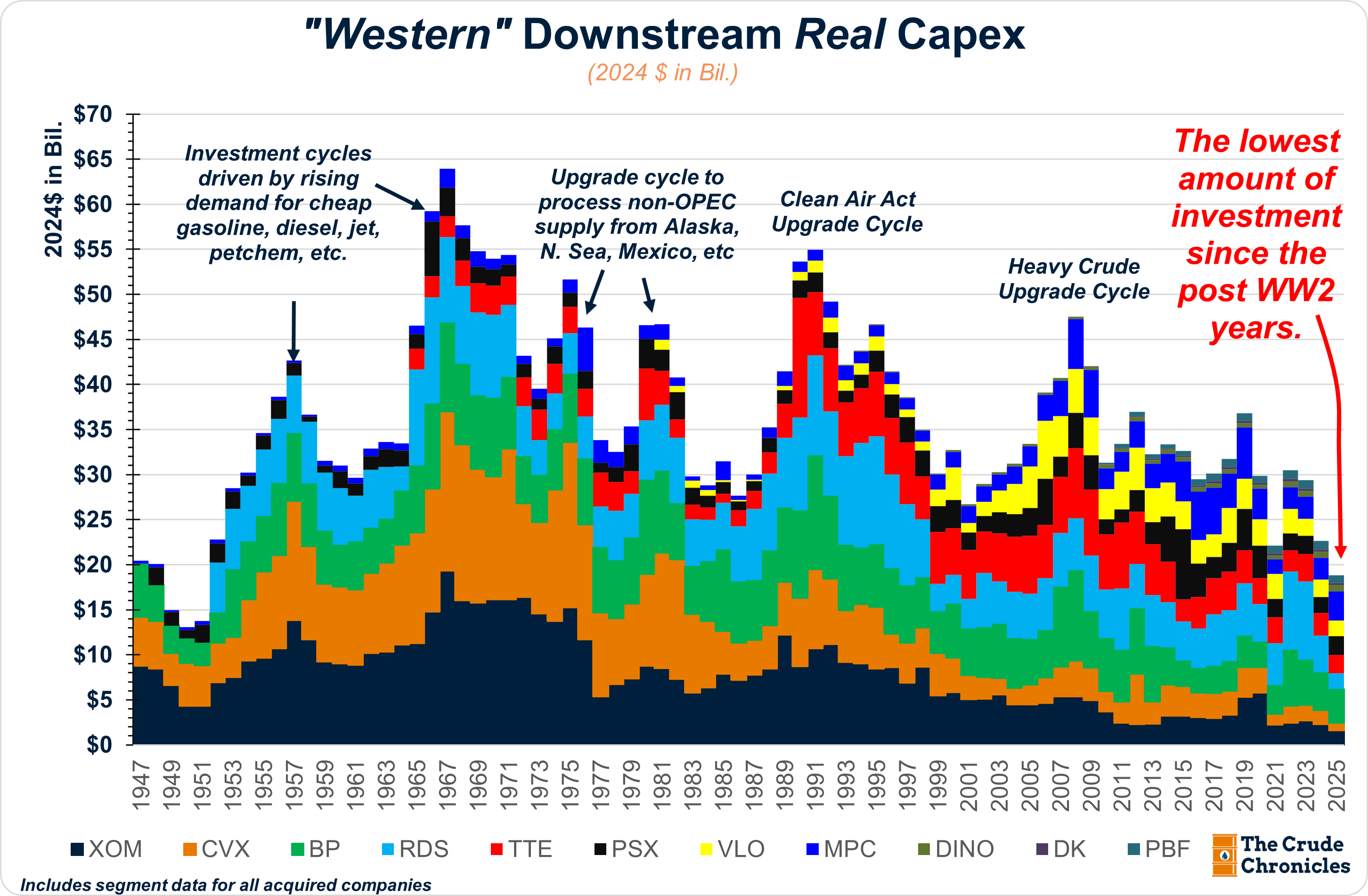

Amongst the O&G sectors, refiners were the first to overspend, but importantly, they were also the first to correct course following the GFC.

Many integrated oil & gas companies spun off their refining operations into standalone entities with their own boards of directors, management teams, balance sheets, and capital allocation frameworks.

What followed was a decisive shift toward capital discipline and shareholder returns.

The rest of the industry has been playing catch-up—with oily E&Ps, U.S. integrateds, and Canadian producers now following suit, while others—namely European integrateds and oilfield services—still have work to do.

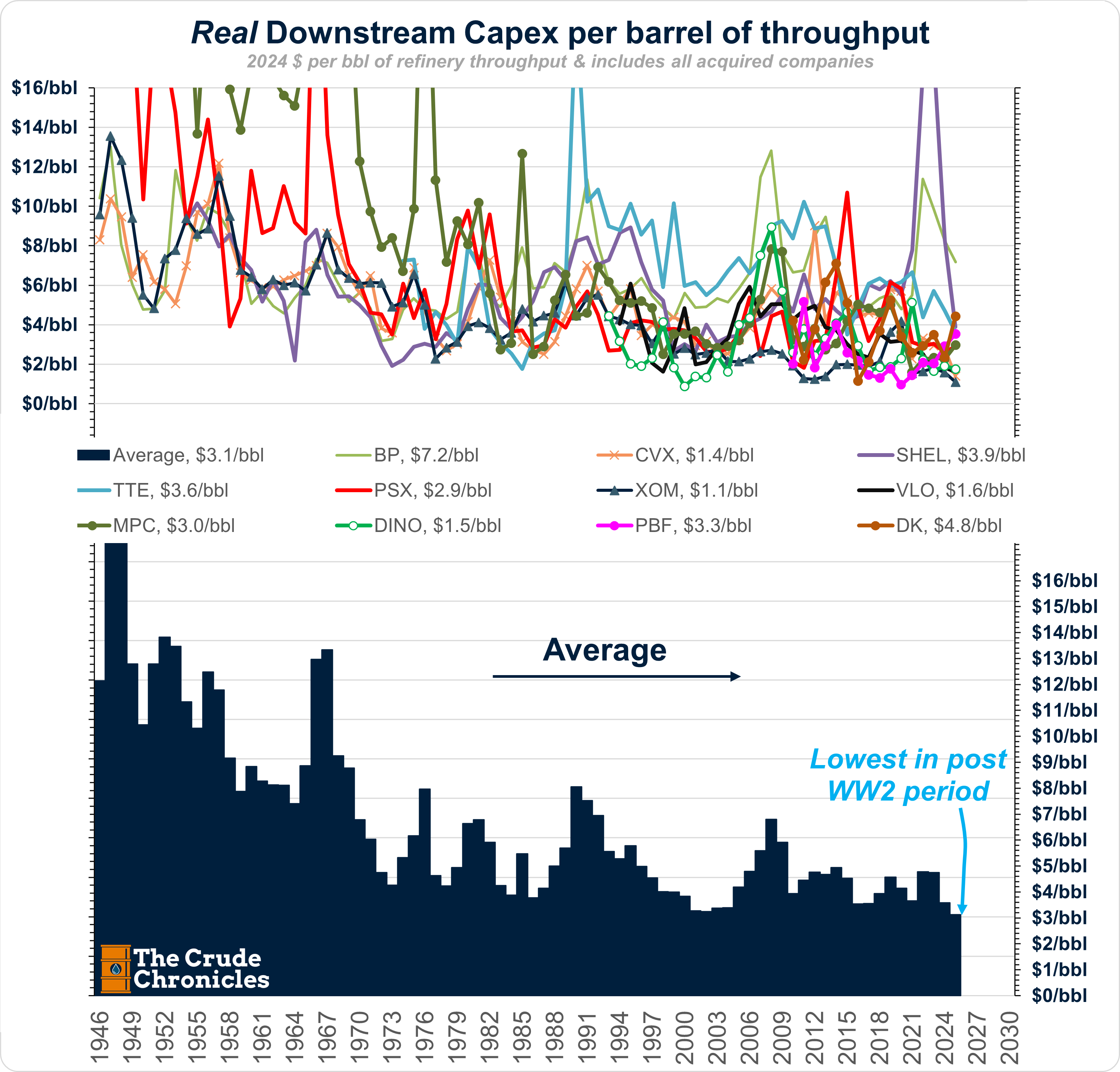

As a result, refiners have become exceptionally efficient. On an inflation-adjusted basis, capex has fallen to post–World War II lows.

The same holds true when normalized on a per-throughput basis.

Investors love refiners because they know exactly what will happen with the cash they generate: buybacks and healthy dividends.

That’s why we’ve said for some time that we prefer “CDUs over GPUs” (HERE).

At the core of this thesis is not just the supply/demand setup—though that matters—but the fact that management teams are incentivized to allocate capital properly, helping ensure the industry avoids another overbuild cycle.

Let’s take a closer look.

In 2025, the four largest publicly traded U.S. refiners generated just over $61 million in realized executive compensation, up 10% year over year.