"Rationalize, Baby, Rationalize!"

The Gist: The U.S. onshore oil & gas service industry faces four structural headwinds: shifting customer behavior, increased leverage by E&P customers over OFS suppliers, technology-driven productivity gains that are rendering the day-rate revenue model less effective in creating value, and rising labor cost pressures. We preview potential solutions.

There are four structural headwinds facing the U.S. onshore oilfield services (OFS) sector.

#1: Customer Behavior Has Changed

The primary headwind is the evolution of E&P incentives.

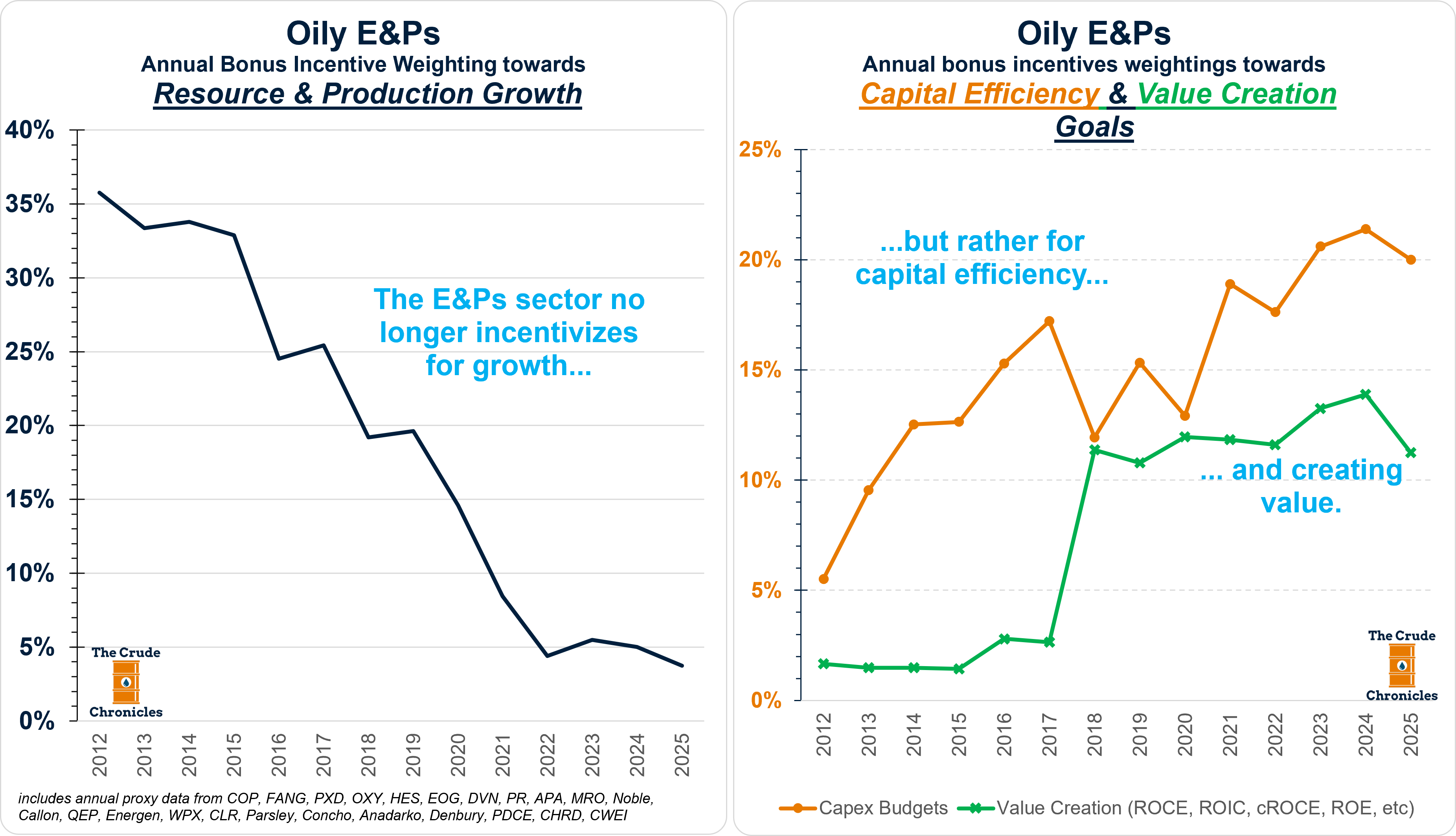

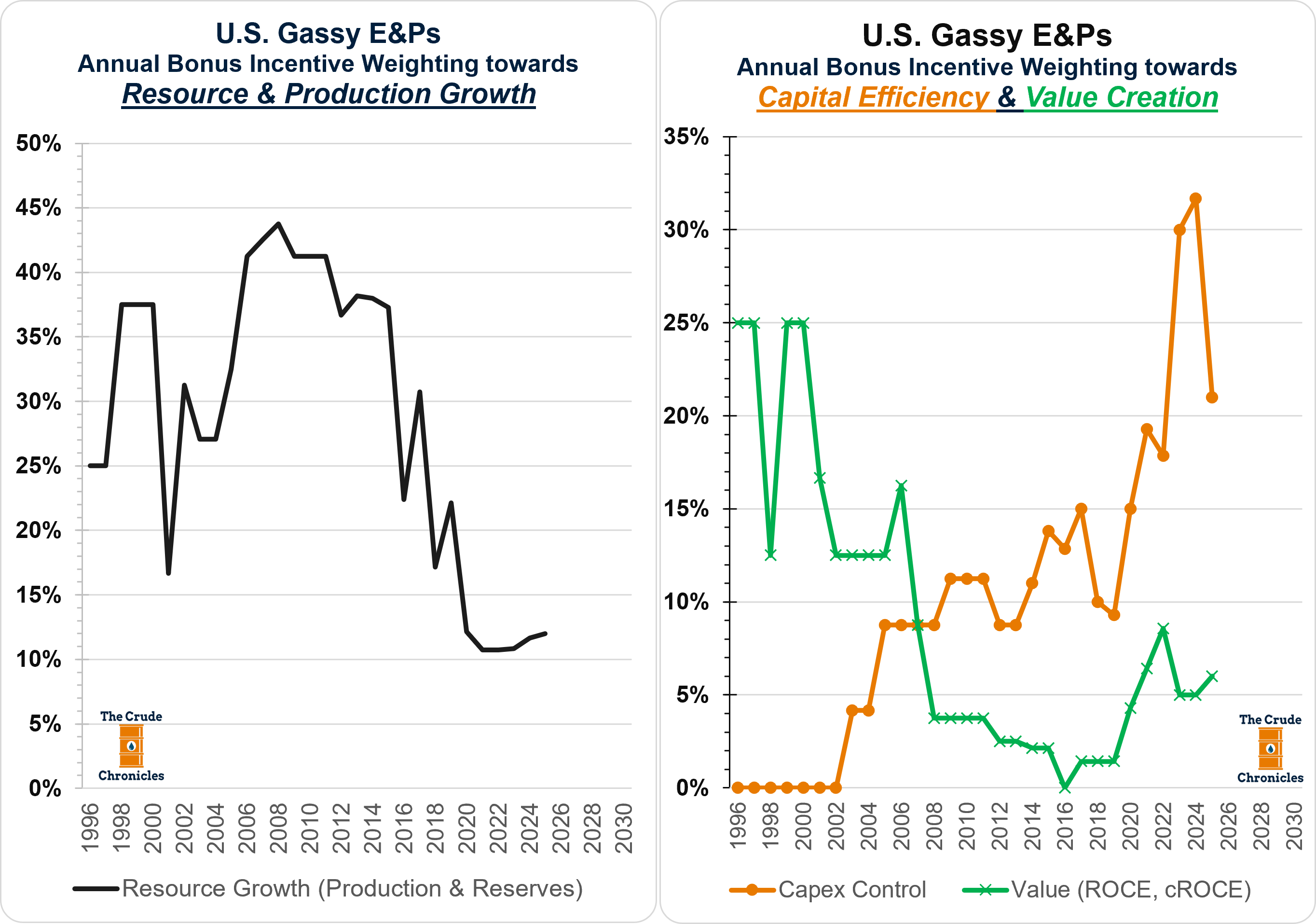

Operators are now focused on capital efficiency and value creation rather than production growth.

This shift is evident across both oily and gassy E&Ps, where incentive structures increasingly reward capital efficiency and value creation over growth.

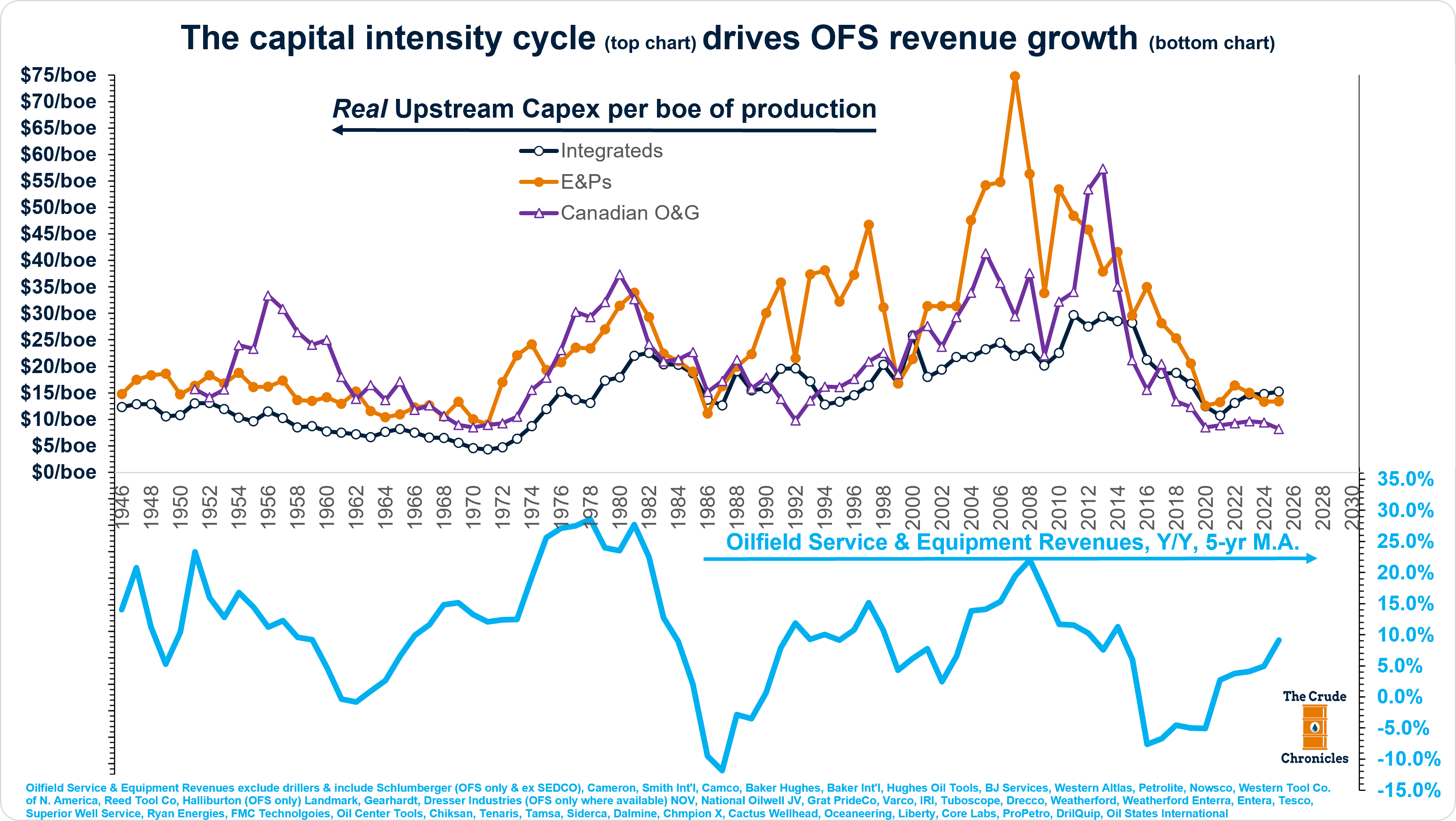

As a result, the capital intensity cycle, which historically drove OFS top-line growth, has been in decline. While a U-shaped bottom may be forming—as F&D costs and marginal costs move higher—the cycle has not yet turned for the service sector.

#2: Structural Pressure on the Drilling Market

The U.S. onshore drilling segment has been the most impacted.

Despite a significant reduction in available capacity, rig utilization remains under pressure.