sPUDing the well

The Gist: The cost to convert PUDs is steadily rising (9% CAGR since 2021). International integrateds are seeing more pressure while U.S. oily E&Ps are rising as well but not to the same extent.

An oil & gas company reports two types of reserves: proved developed (PD) and proved undeveloped (PUD).

Proved Undeveloped (PUD) are reserves that are confirmed to exist, but require new wells and future capital investment to reach production.

Beginning in 2014, SEC rules were updated so that only PUDs expected to be developed within five years can be classified as such.

Proved Developed reserves (PD) are further along the value chain. These reserves can be produced using existing wells and infrastructure with capital having largely been spent.

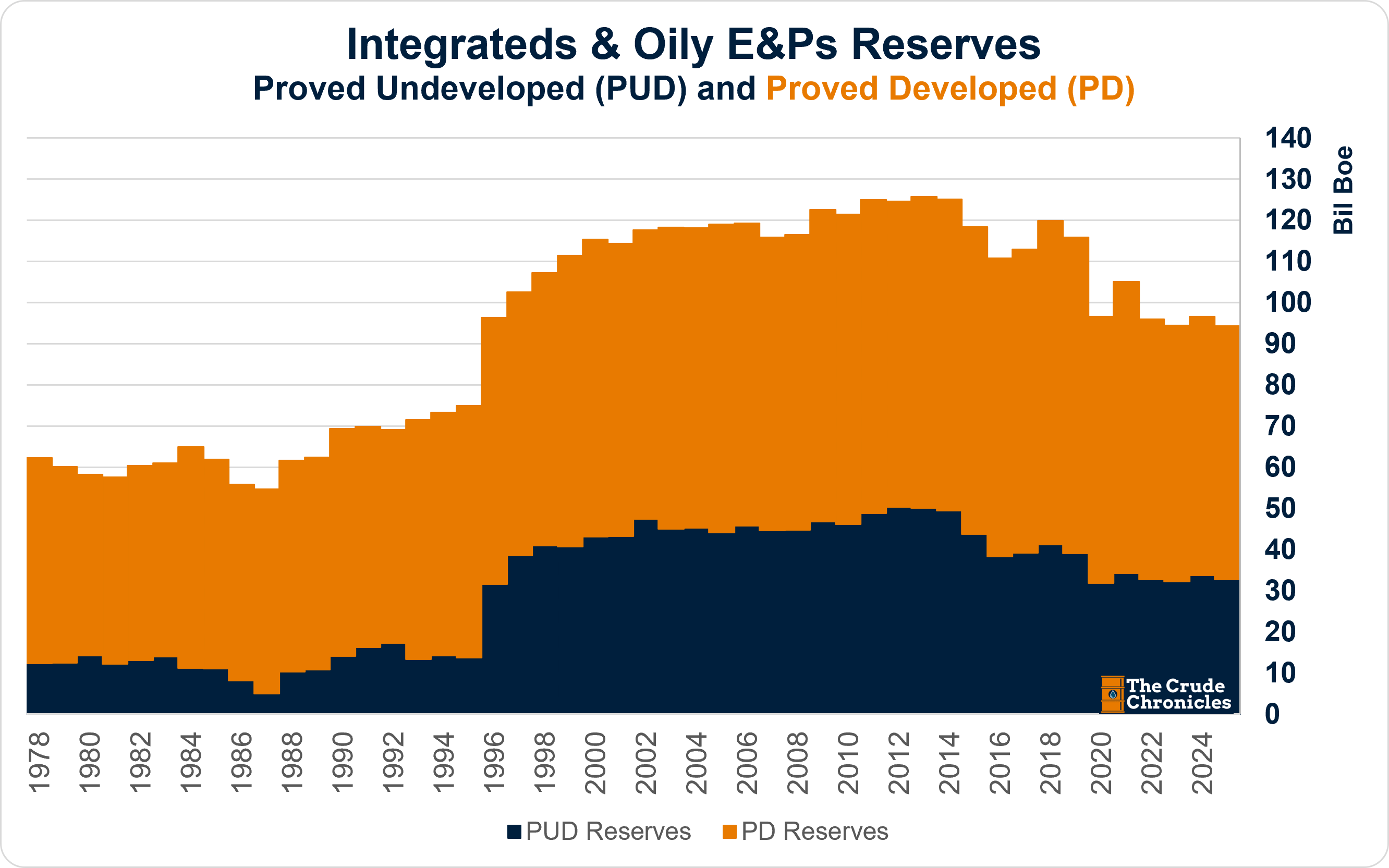

Together, PUD + PD = Proved Reserves (1P).

In addition, there are Probable Reserves, which are less certain but still likely to be recovered. Under U.S. SEC rules, these are not included in official filings, but in other jurisdictions—such as Canada—they are disclosed. Russian regulators have even more levels of reserve classifications.

In industry terms, Probable Reserves are referred to as 2P.

A simple way to think about it:

Probable → PUD → PD → Production

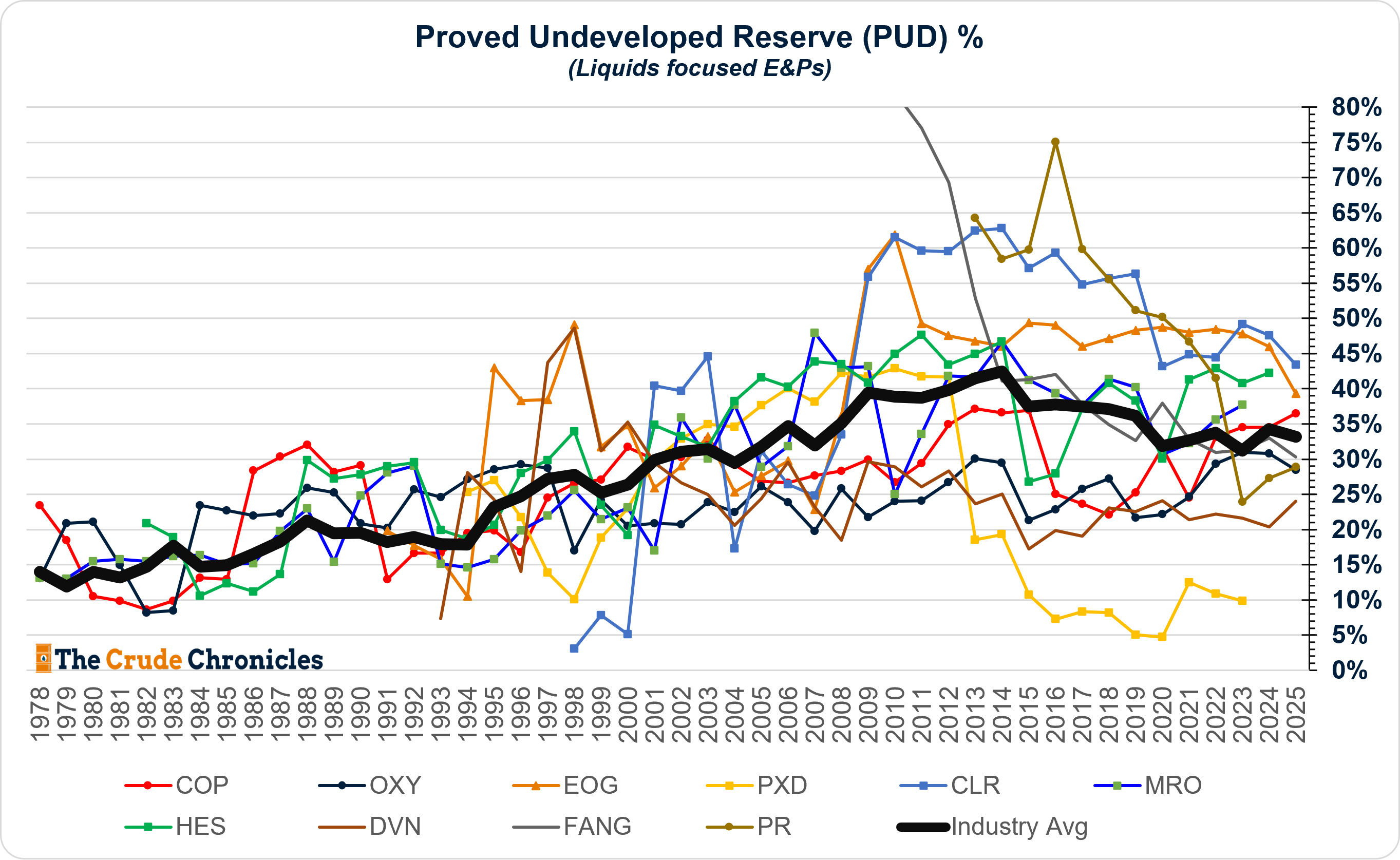

PUD % for the oily E&Ps look like such.

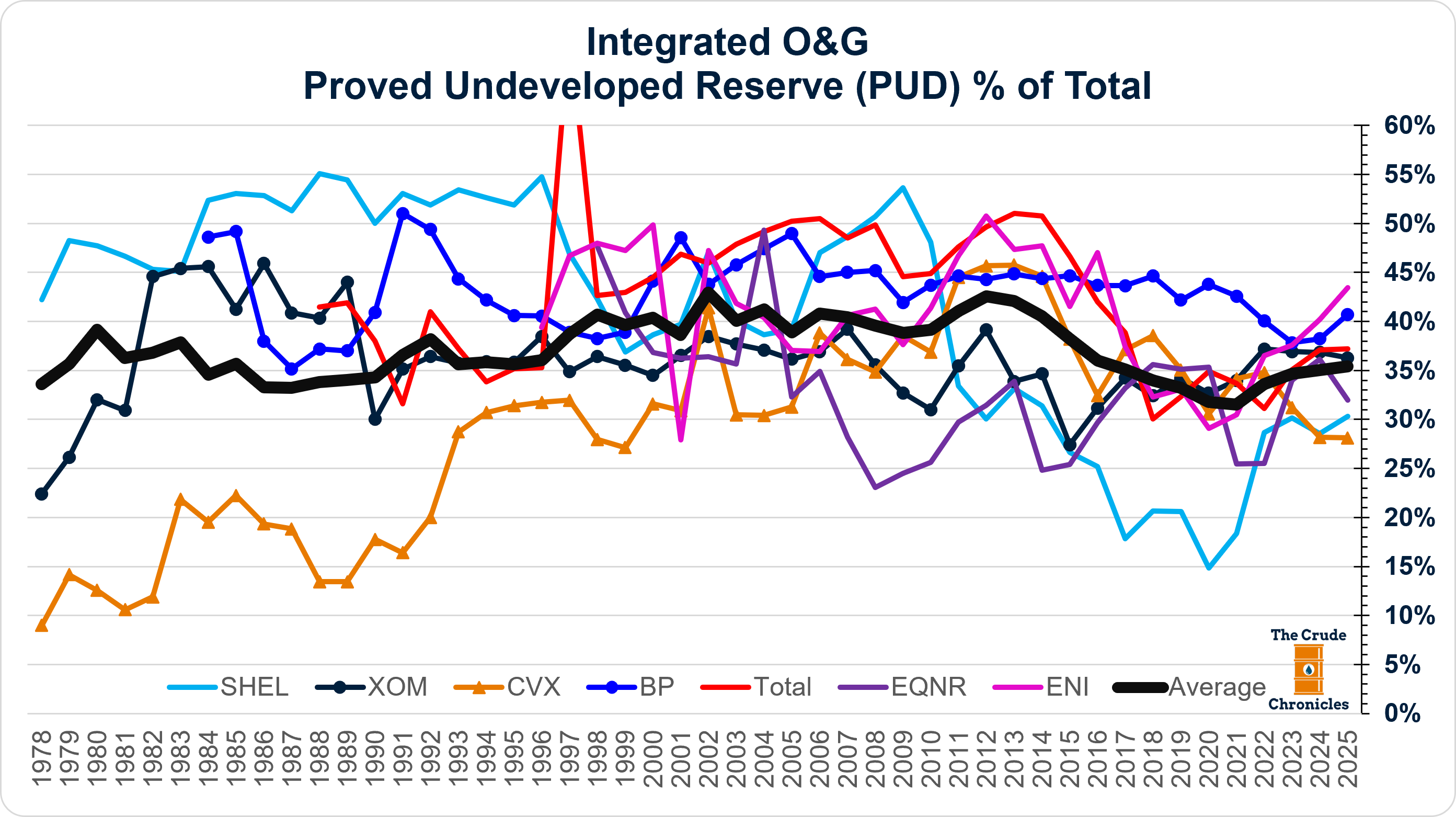

And the integrated oil & gas names are as follows.

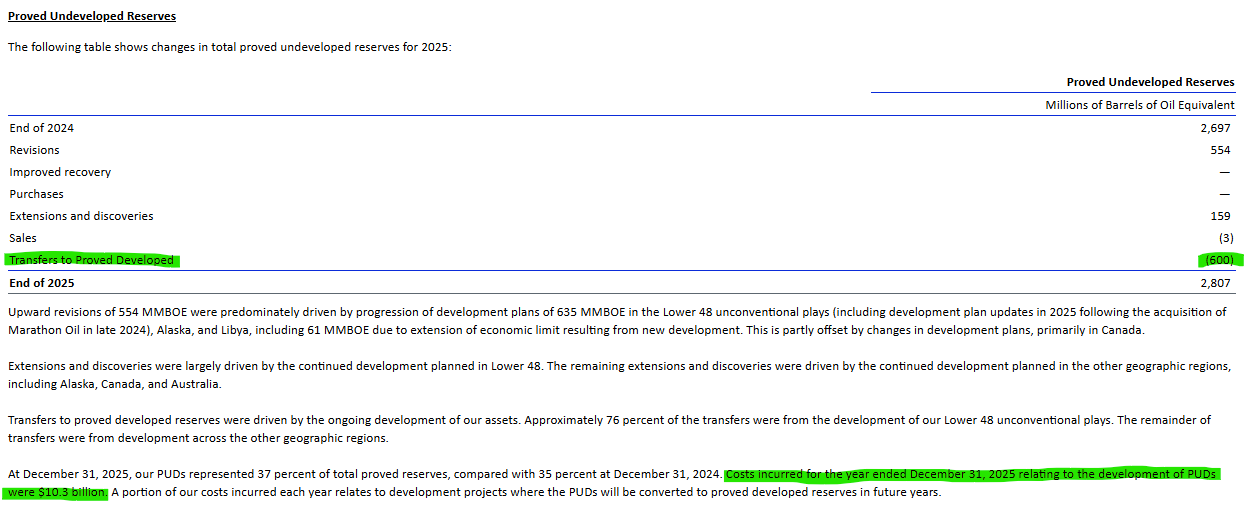

Every year, oil & gas companies disclose how much of their reserves were converted from PUD to PD, as well as the capital required to make that conversion. This disclosure is required under SEC reserve reporting rules and provides investors with a useful measure of both capital intensity and development progress.

Below is an example from ConocoPhillips’ latest 10-K.

At the industry level, an increasing percentage of PUDs are progressing into the PD category, now exceeding 20%. However keep in mind from the first chart in this post that PUDs are just staying level.