The Chinese O&G SOEs

The Gist: (1) China’s state owned O&G companies can’t be ignored, they produce a lot of boe and their ROCEs are comparable to their Western peers. (2) The upstream side of the business drives their returns despite producing a more capital intensive molecule. (3) These companies are massive in downstream but the U.S. refining is a better business for shareholders. (4) Bonus: a sneak peak into the global capex data I am collecting.

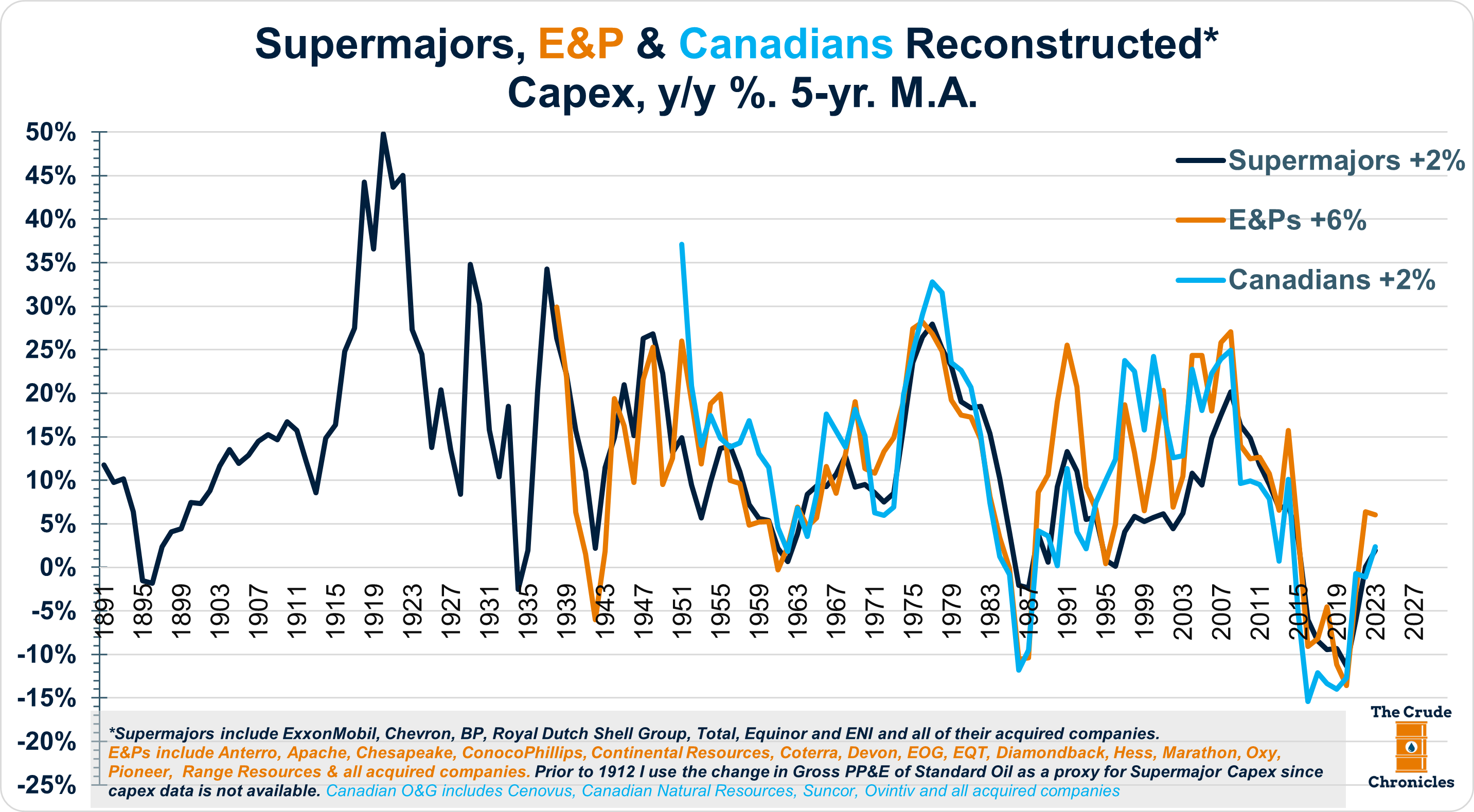

The push back I often get with my historical capital spending (capex) charts like the one below is “You don’t have the national oil companies (NOCs).”

So I have made it a mission of mine to gather as much publicly available data from the various NOCs.

My journey around the world takes me to China and its state-owned enterprises (SOEs) in the Oil & Gas sector. There are three main ones that will be the focus of this post (see the bottom of the post for a brief recap/history of the three SOEs).

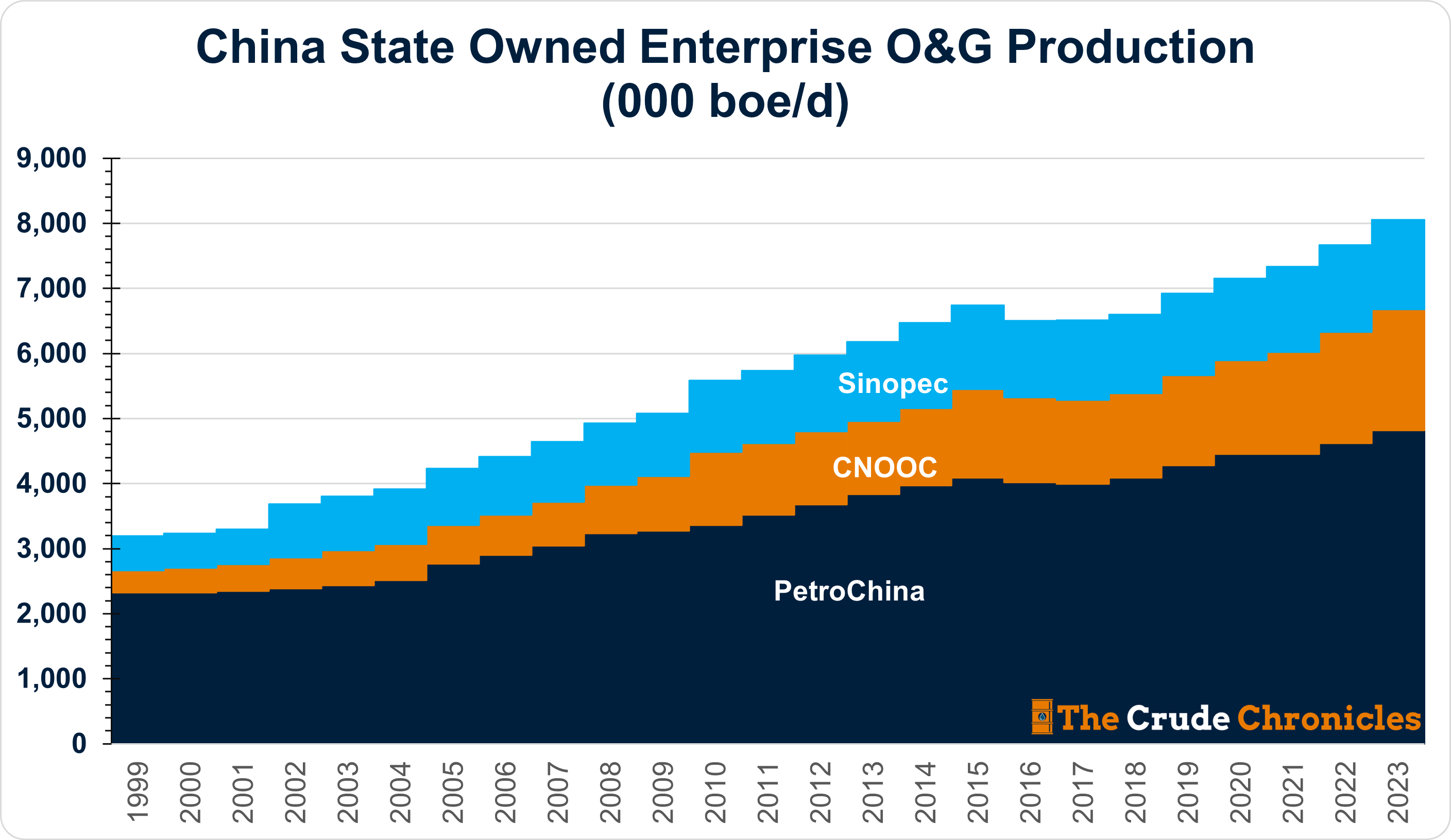

Despite China's challenging geology and petroleum import dependece, these companies have managed to increase production from 3 million barrels of oil equivalent per day (boe/d) at the turn of the century to 8 million boe/d in 2023.

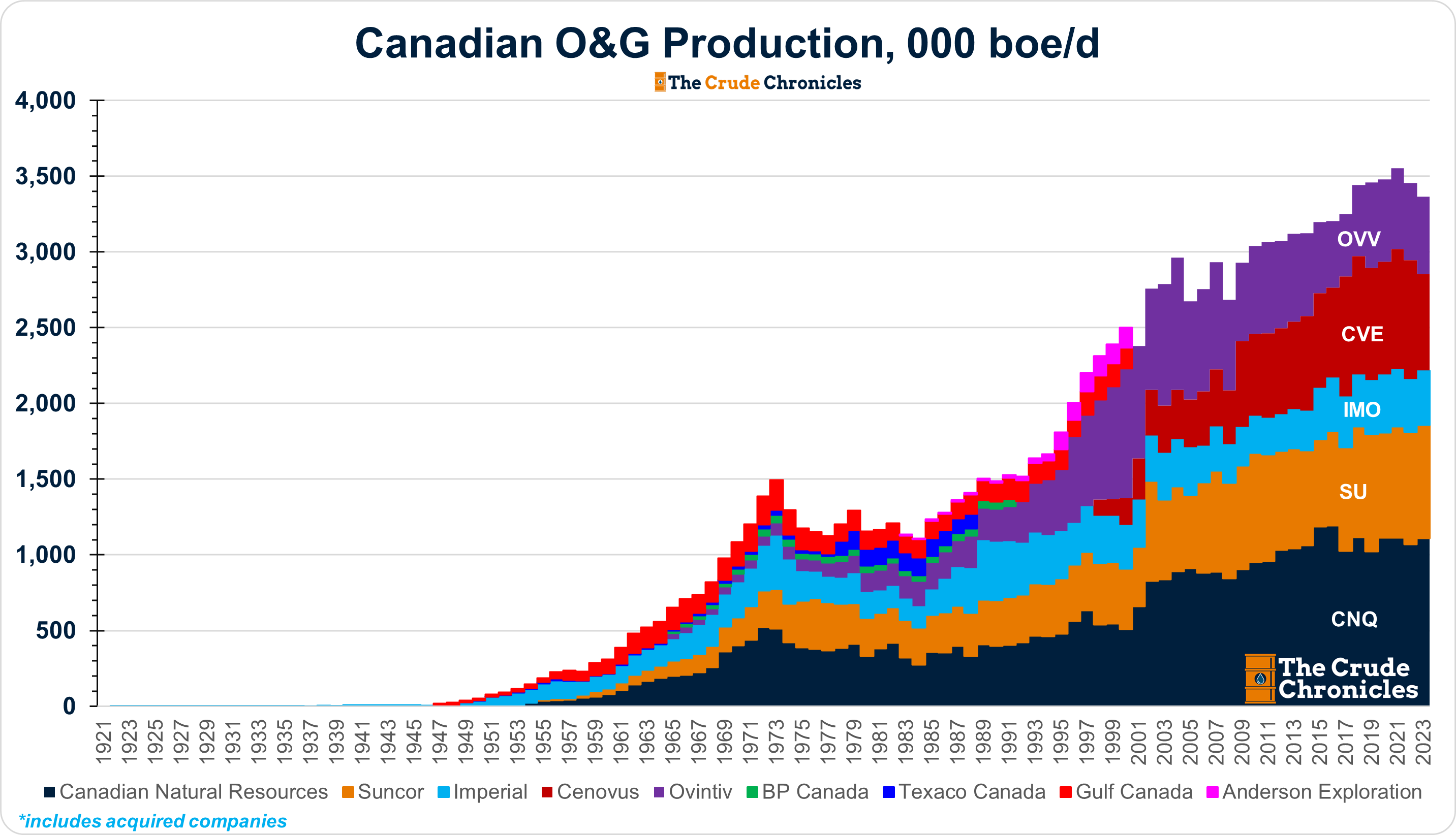

For anyone that is counting, 8mil boe/d is larger than the Big 5 Canadian O&G names.

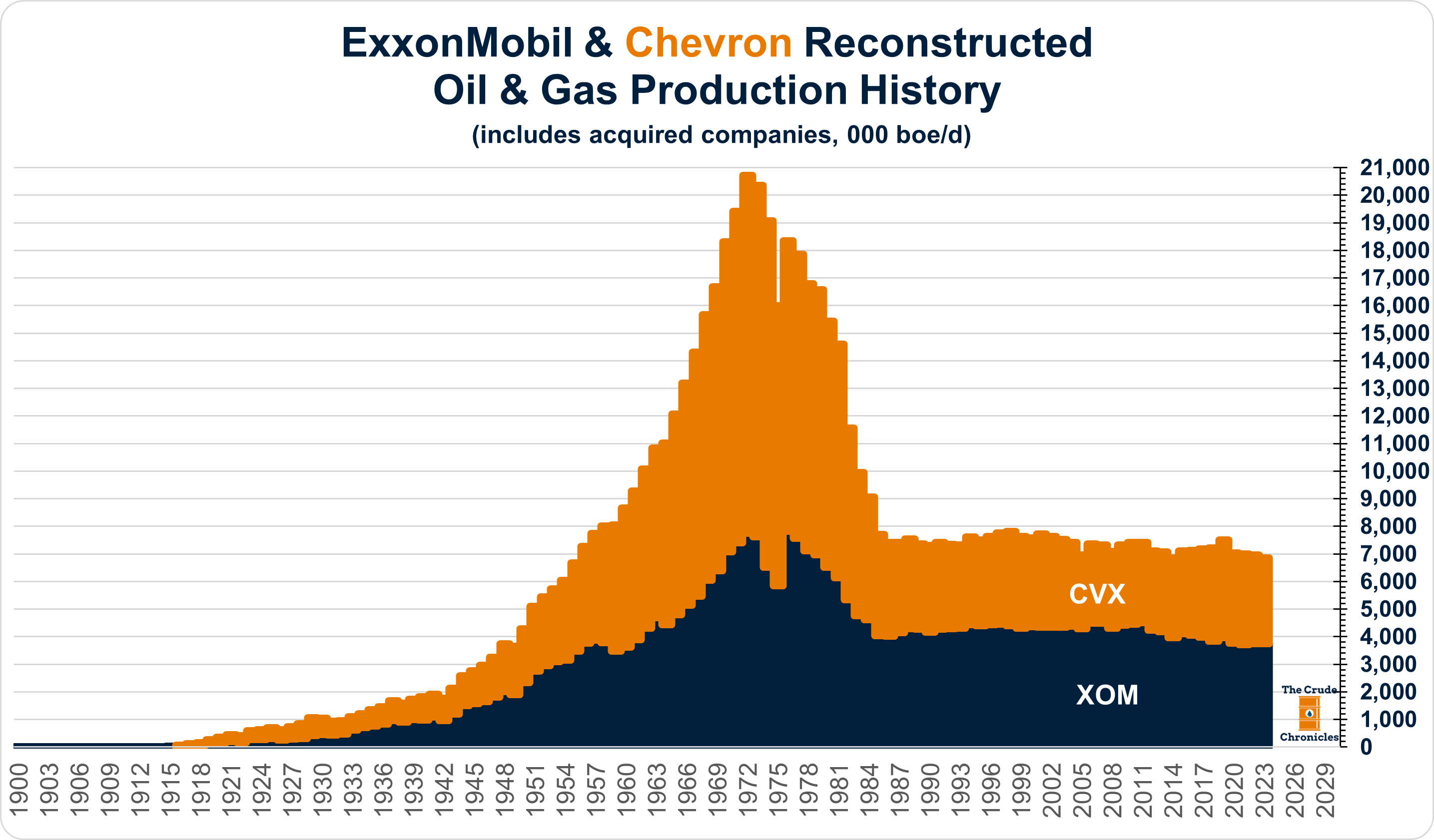

And 1 million boe/d more than XOM and CVX, the two integrated oil companies that most western investors own these day.

Albeit the above chart does not include the Pioneer and Hess transactions.

Despite being state owned entities the Chinese O&Gs return on capital profiles are eerily similar to that of their Western peers.

Keep reading with a 7-day free trial

Subscribe to The Crude Chronicles to keep reading this post and get 7 days of free access to the full post archives.