The Energy Transition & Freeport-McMoran's History

The Gist: The first half of this post shows the energy transition is occurring everywhere but in the market for copper and its producers such as Freeport McMoran. The second half of this post is a brief financial history of the company.

To paraphrase Robert Solow, “you can see the energy transition everywhere but in the copper price. “

If we were moving towards a worldwide electrification of power and transportation needs, one would assume copper prices would be outperforming various other financial assets, the S&P included. However, that is not the current situation.

In such a scenario, one would also expect that copper prices would be outpacing oil. Yet, once again, that assumption does not hold true.

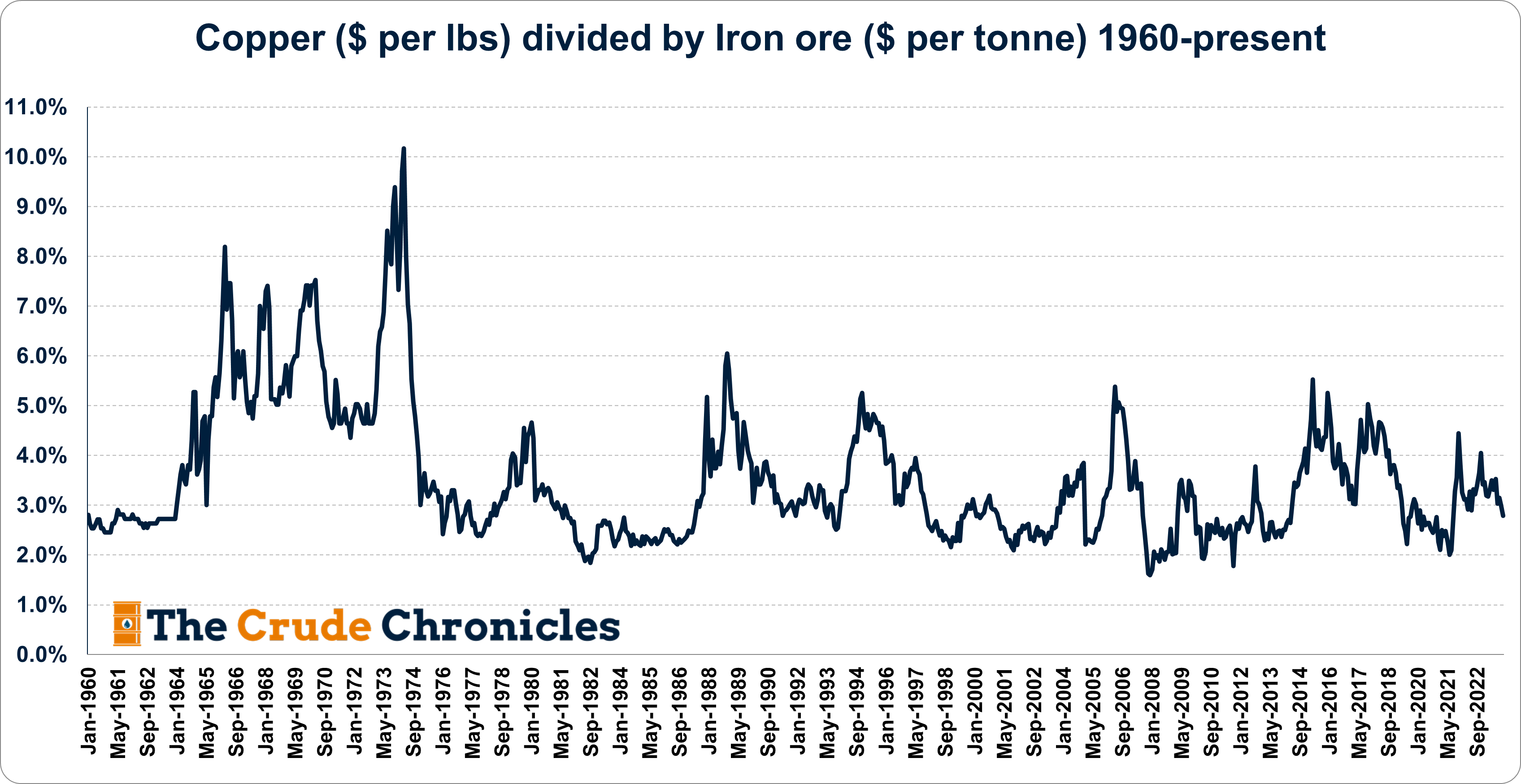

The counterargument might attribute the weakness in copper to the construction downturn in China.

However, the ratio of copper to iron ore, which serves as an indicator of electrification versus construction, does not display an upward trend consistent with any identifiable theme related to the energy transition.

Why does all this matter for a company like Freeport?

Because, as one would expect, copper inflation cycles drive returns on capital.

But returns are in the past and stocks are a future discounting mechanism.

Yet here again, we do not see any sort of multiple expansion occurring as had in the past for FCX and its predecessor Phelps Dodge.

Keep reading with a 7-day free trial

Subscribe to The Crude Chronicles to keep reading this post and get 7 days of free access to the full post archives.