The PBoC is doing its part to prime the GM2 Oil Pump

The PBoC is doing its part to prime the GM2 Oil Pump

The Gist: The post on Tuesday was about the long-term drivers of oil prices (HERE). Today’s post discusses the cyclical drivers. (1) Global money supply (GM2) has some gas in the tank, driven by China's stimulus and a weakening dollar, both of which are bullish oil. (2) However, there are risks the U.S. credit cycle disappoint later this year which would take the wind out of oil’s sails.

Almost 2 months ago in my post titled, “It's not the Houthis it's the SHIBORs!” (HERE) the point was made that “China appears to have a deflation problem on its hands and responding with increased stimulus which could strengthen domestic M2, and provide liquidity for oil.”

Since that time the PBoC has continued to respond with even more policy support and markets are starting to notice with the consensus moving towards a more optimistic outlook for China.

But first some monetary plumbing.

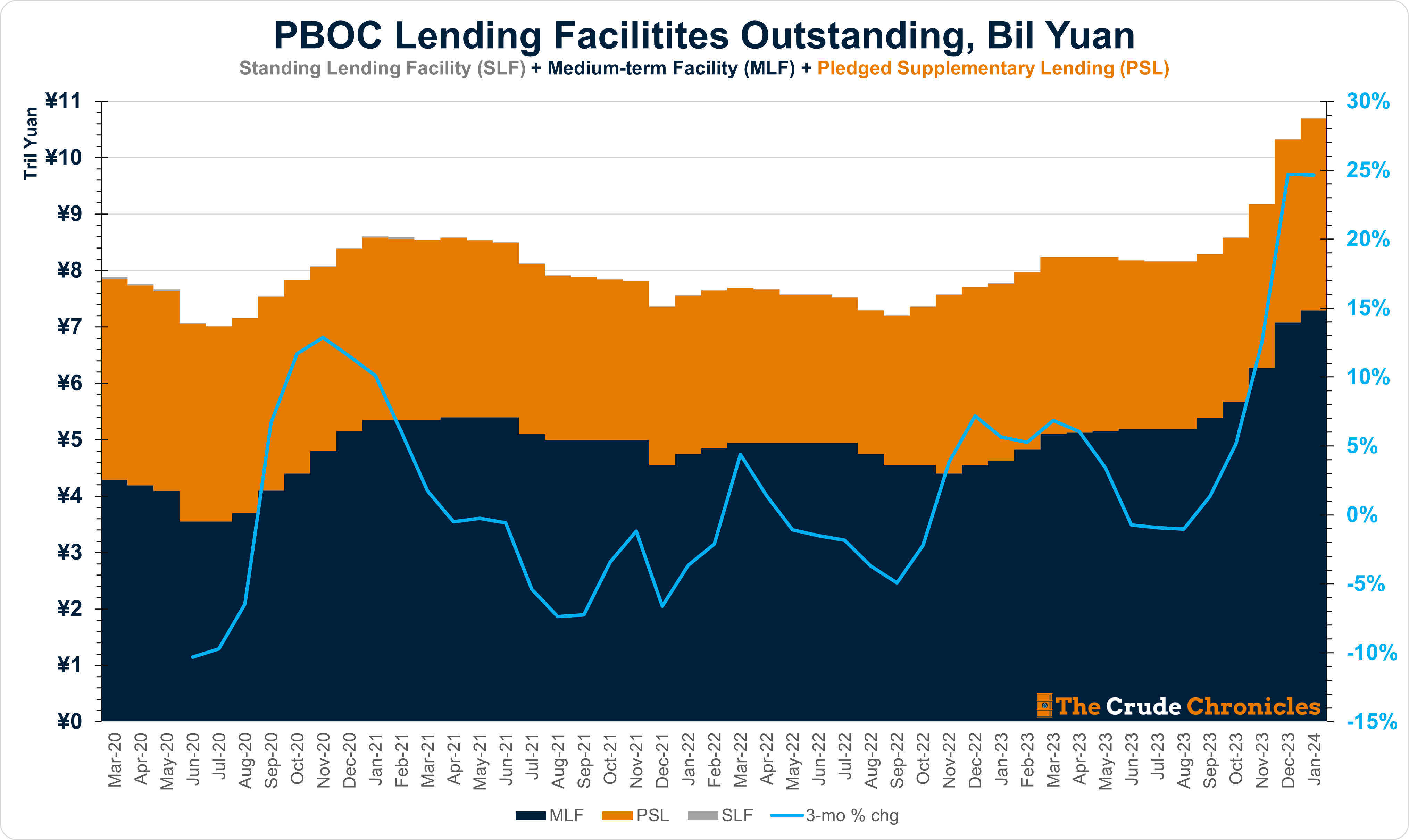

There are two main items on the PBOC’s balance sheet; foreign exchange reserves and a line item titled Claims on Other Depository Corporations.

The former is used to manage the currency while the latter is used to provide policy support to the economy. The latter is blowing out as shown below.

The last time they provided this much liquidity was in 2016 as the central bank was attempting to stave off an interbank liquidity crisis but this time, the money markets in China look fine.

This support is provided through lending facilities such as the PSL and MLF which are used to direct credit to select areas of the economy. These lending facilities have continued to expand rapidly as well.

In addition, lending spreads are widening which tends to be positive for China's money supply.

Keep reading with a 7-day free trial

Subscribe to The Crude Chronicles to keep reading this post and get 7 days of free access to the full post archives.