MRO/COP, Stage 3, & then there were 3

MRO/COP, Stage 3, & then there were 3

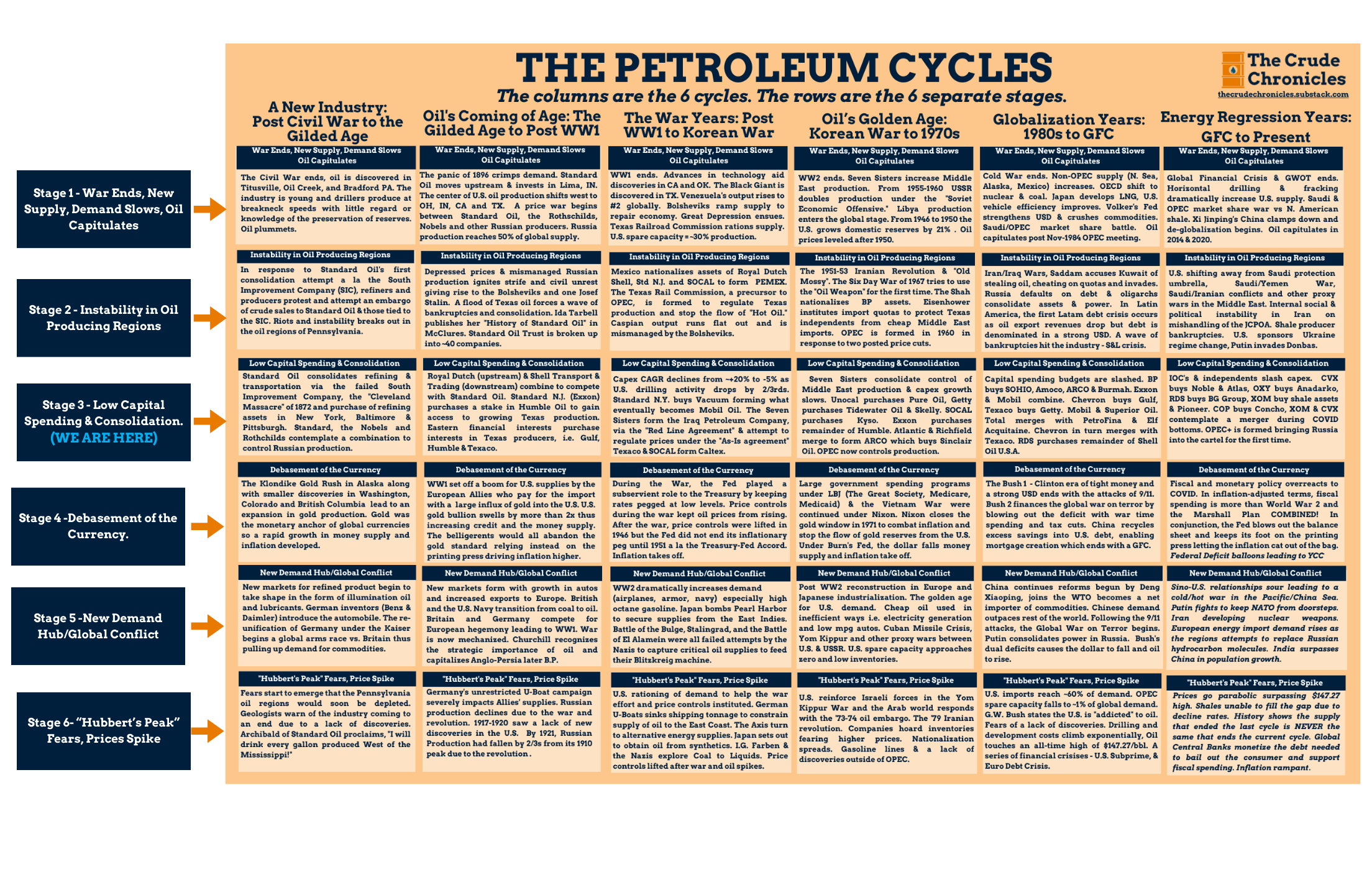

The COP & MRO combination clearly shows we are in the later part of stage 3 (typically 6 stages) of the Petroleum Cycle. (2) Companies are taking a page out of the late 1990s playbook and being rewarded for it. (3) As a final tribute, the rest of the post is a brief financial overview of "The Ohio Oil Company."

With ConocoPhillips continuing the wave of M&A by acquiring Marathon, it is clear that we are in the midst of Stage 3, as shown below.

A free PDF version is below.

If history continues to repeat itself, Stage 4—Debasement of the Currency—is next, followed by Stage 5—New Demand Hub/Global Conflicts. Finally, in Stage 6, the current narratives around “peak demand” will transform into narratives around “peak supply.” Rinse and repeat.

There were 34 companies created after Standard Oil was broken up, most of them being pipeline, midstream, and storage companies. (HERE).

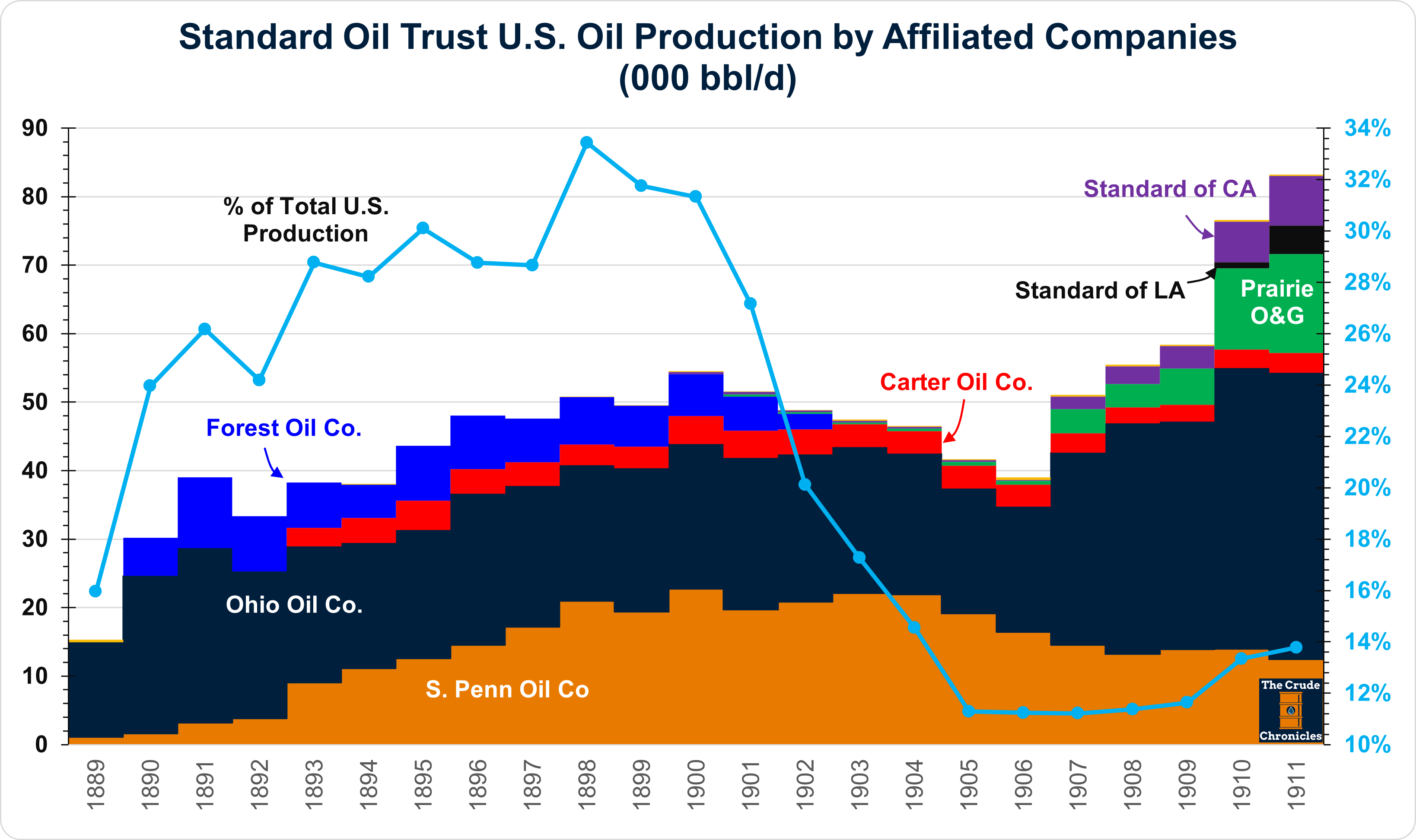

In the beginning, Marathon was an E&P company previously named “The Ohio.” It was Standard Oil's first foray into the upstream side of the business when Rockefeller purchased the company in 1889. It quickly became the largest producer in the state as well as within the Trust.

Conoco (formerly Continental Oil) was primarily composed of the Mid-Con marketing assets of Standard Oil. Phillips Petroleum never fell under the control of the monopoly, as Frank Phillips fought to keep the company independent even through the Great Depression (HERE).

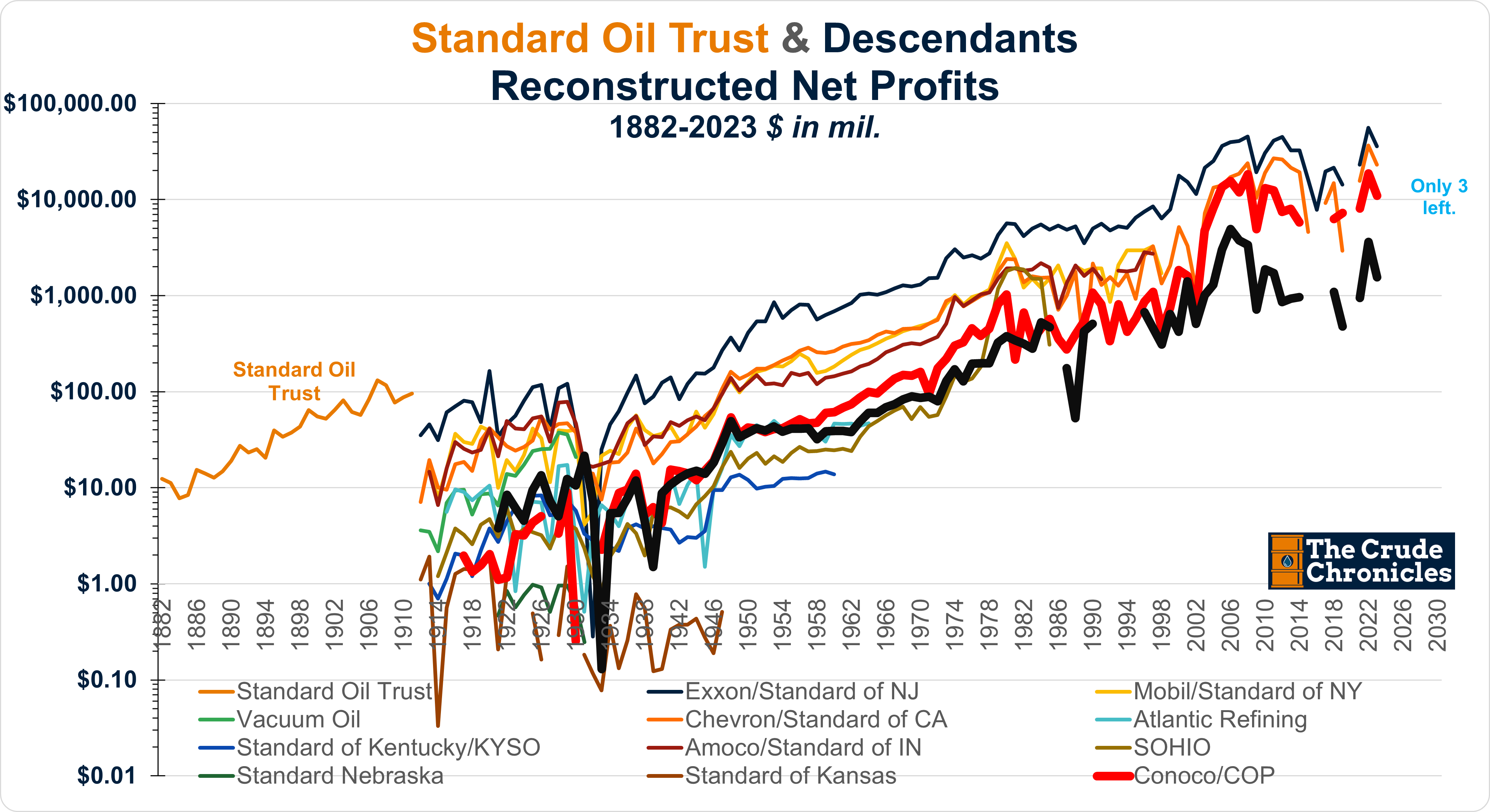

Fast forward to today, and out of the 34 companies that emerged from the breakup, only 3 remain.

Throughout COP’s history, the company’s production has tended to stay concentrated in what I would term the "OECD Developed World," primarily including the US, Canada, and Europe.

Keep reading with a 7-day free trial

Subscribe to The Crude Chronicles to keep reading this post and get 7 days of free access to the full post archives.